Geomechanics, Streamlined.

© 2026 Geomechanics.io. All rights reserved.

Overnight northbound closures will affect the M80 between Junctions 7 and 9 every Monday to Friday and most Sundays until 6 July, as gantry replacement works proceed under full carriageway shutdown. Transport Scotland and its contractors are moving to closures after thousands of drivers ignored temporary speed limits through the works, increasing risk to crews operating adjacent to live lanes. The change will concentrate heavy lifting, lane marking and electrical works into night-time windows but may push more HGV and commuter traffic onto local A‑roads during closure hours.

Mott MacDonald has agreed to acquire Australian civil contractor Leed Engineering & Construction, expanding its capability to deliver water, transport and energy infrastructure across metropolitan, regional and remote areas. The deal adds a self-perform construction arm to Mott MacDonald’s existing design and advisory business in Australia, enabling integrated design-and-build delivery on complex civil works. For geotechnical and civil practitioners, the move signals more bundled packages where ground investigation, detailed design and construction of pipelines, bridges and treatment assets are procured from a single team.

Defra and Natural England have launched a call for evidence, open until 22 May 2026, asking developers and construction contractors to share practical experience of great crested newt protection on housing and infrastructure schemes. Supported by consultants LUC and ICF, the review targets on-site measures such as exclusion fencing, pitfall trapping, seasonal timing of earthworks and licensing delays. Responses could influence future mitigation licensing, survey requirements and design-stage constraints on sites where newt habitats intersect with foundations, drainage and earthworks.

King Charles III’s first King’s Speech under the new Labour government offered almost no concrete legislative detail for construction or infrastructure, leaving professional bodies such as RIBA and CIOB largely underwhelmed. Representatives from the Residential Freehold Association and Churchill Living also struggled to identify clear implications for planning reform, building safety, or long-term capital investment. For engineers and contractors, the absence of specific commitments on housing delivery targets, infrastructure pipelines, or regulatory changes signals continued policy uncertainty heading into 2025.

First Quantum Minerals has filed an NI 43-101 Technical Report with an updated copper Mineral Resource estimate for the La Granja project in northern Peru, where it holds 55% alongside Rio Tinto’s 45% stake. The development concept leaves corridor and power design flexibility for future trolley-assist haulage, signalling potential partial electrification of the truck fleet on the steep pit ramps. For mine planners and geotechnical teams, early allowance for trolley lines, substations and ramp geometry could materially influence slope design, haul profiles and overall pit layout.

Sandvik Ground Support has agreed a US joint venture with Alpha Metallurgical Resources to establish local manufacturing for rock reinforcement products, with Sandvik holding 51% and Alpha 49%. The structure includes a long-term exclusive supply arrangement, giving Sandvik secured offtake into Alpha’s underground coal operations while anchoring domestic production capacity for bolts, mesh and other ground support consumables. For US mines, the move signals shorter supply chains, reduced import exposure and potentially tighter technical integration between support design and production.

Government plans to nationalise British Steel aim to preserve domestic production of structural sections, plate and rail steel used in major UK infrastructure, but raise questions over long‑term subsidy levels and exposure of public finances. Civil contractors reliant on BS EN 10025 and BS EN 10210 compliant sections could see short‑term supply stability, yet face potential cost volatility if state ownership drives changes in pricing, energy cost pass‑through or decarbonisation investment. The move also concentrates risk for large public works pipelines such as HS2, road bridges and offshore wind foundations.

The £34.8M decarbonisation programme at Nottingham City Hospital, the UK’s last coal-heated hospital, has eliminated 16,000t of carbon emissions and is delivering £1.4M in annual energy savings. Works included replacing coal-fired plant with low-carbon heating and power systems, alongside extensive upgrades to building services and controls. For engineers, the project shows the scale of carbon and cost reduction possible from deep retrofit of legacy NHS energy infrastructure.

South Staffordshire Plc and South Staffordshire Water Plc have been fined £963,900 by the Information Commissioner’s Office after a 2022 cyber-attack compromised their IT systems and exposed customer data. The incident affected corporate networks rather than process control, but it raised concerns over the segregation and resilience of operational technology supporting water treatment and distribution assets. Water utilities and other infrastructure operators are likely to face closer scrutiny of cyber-security for SCADA, telemetry and remote monitoring systems, with potential implications for future asset management and capital upgrade programmes.

BBV has completed assembly of HS2’s tallest bridge, Curzon 2, ahead of its planned weekend launch over a live rail corridor in central Birmingham. The structure, part of the Curzon Street station approaches, will be installed during a tightly constrained possession window over a busy existing line, requiring precise control of lift tolerances and rail clearance. For civil and geotechnical teams, the operation centres on managing crane outrigger loads, ground bearing pressures and real‑time monitoring to protect adjacent track and signalling assets.

Transport Infrastructure Ireland has launched procurement for the largest contract on Dublin’s £8.4bn (€9.5bn) MetroLink, covering rolling stock supply, core railway systems and full station fit-out. The package also includes a 25‑year operations and maintenance concession for the driverless metro service, bundling lifecycle responsibility for trains, signalling, power and platform systems. The scale and duration of the contract point to long-term performance-based requirements on systems integration, reliability and maintainability for contractors and their supply chains.

King Charles’s 2026 speech sets out bills aimed at unlocking UK airport expansion and accelerating major transport infrastructure construction. Measures are expected to streamline planning and consenting for runway extensions, terminal upgrades and associated surface access works, and to simplify approvals for large rail and highway schemes. Civil and geotechnical engineers should anticipate tighter programme windows, earlier ground investigation and design commitments, and greater emphasis on integrating airfield works with surrounding road and rail capacity upgrades.

A temporary weight limit will be imposed on London’s Vauxhall Bridge from 1 July to “ensure safety for all bridge users”, signalling concern over current load effects on the early-20th-century steel and granite structure. While the exact tonnage has not been disclosed, the restriction will immediately affect heavy goods vehicles and abnormal loads using this key Thames crossing on the Inner Ring Road. Asset managers and bridge engineers will be watching for follow‑on measures such as detailed structural health monitoring, lane loading changes, or accelerated strengthening works.

Four mining technologies from the ARC Training Centre for Integrated Operations for Complex Resources are now ready for field trials, including a digital twin platform for complex orebodies, real-time sensor fusion for ore characterisation, and AI-based decision support for integrated mine-to-mill control. The suite targets data-driven optimisation of drilling, blasting, and processing, with pilots seeking partners across hard-rock operations and brownfield plants. For engineers, the work signals near-term opportunities to plug advanced analytics and automation into existing fleets and control rooms without full greenfield redesigns.

Motion is deploying in-situ machining services to Australian mine sites, bringing line-boring, flange facing and journal repair directly to assets such as car dumpers, draglines and large gearboxes that are too large or time-critical to dismantle. Using portable CNC and orbital machining rigs, technicians can restore bearing seats, slew rings and mill trunnions to tolerance without removing them from foundations or structural frames. The approach reduces crane lifts and transport of multi-tonne components, cutting outage durations and geotechnical or structural risk associated with repeated disassembly.

Australian Power Equipment is reframing mine-site optimisation around transformer reliability, availability and lifecycle performance rather than lowest upfront cost, supplying B&D transformers filled with FR3 natural ester fluid instead of mineral oil or diesel-based coolants. The FR3 ester offers higher fire point and biodegradability, enabling compact substation layouts closer to plant and reduced bunding requirements, which can simplify brownfield expansions. For engineers, the shift pushes whole-of-life asset modelling, factoring in longer insulation life, fewer unplanned outages and reduced supply chain risk for critical electrical equipment.

Equinox Gold’s US$18.5 billion acquisition of Orla Mining will create a North America-focused gold producer targeting 1.1 Moz/year initially, with a development pipeline that could lift output about 70% to 1.9 Moz/year. The combined portfolio will span operating and growth assets in Canada, the US, Mexico and Nicaragua, including the Greenstone and Valentine projects plus Orla’s Musselwhite mine, with Equinox CEO Darren Hall staying as chief executive and Orla’s Jason Simpson becoming president. The new entity will also assume Orla’s roughly US$400 million arbitration claim over the stalled Cerro Quema project in Panama.

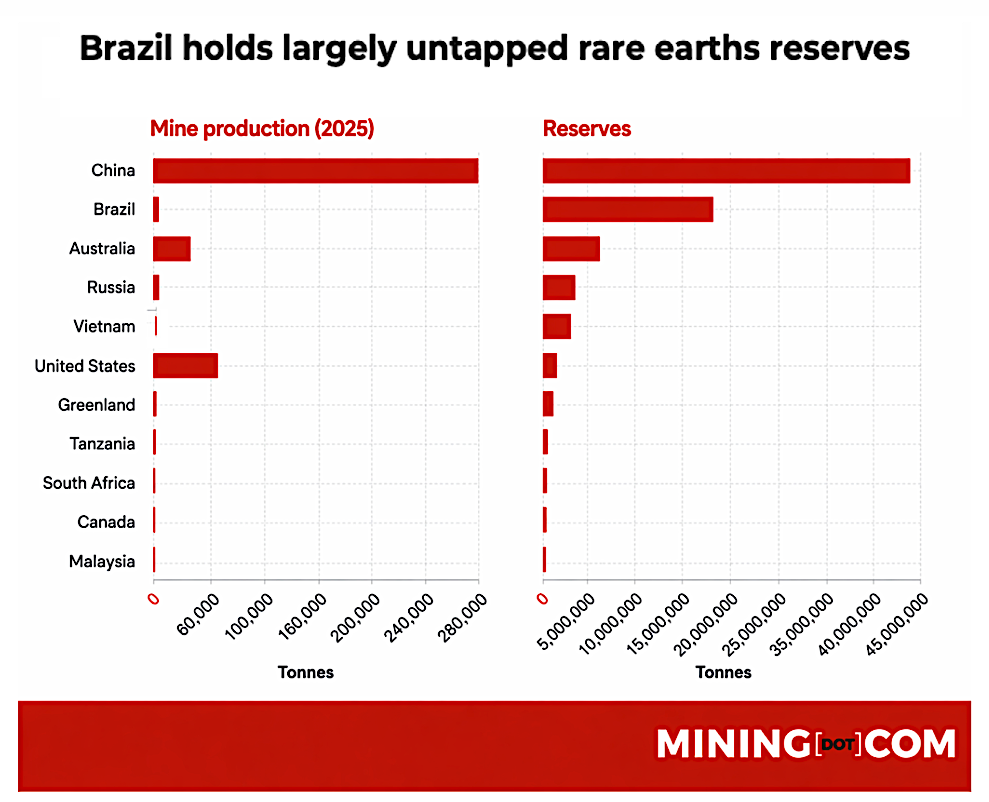

US President Donald Trump and Brazil’s Luiz Inácio Lula da Silva are using rare earths to recalibrate ties, centring talks on USA Rare Earth’s proposed $2.8 billion acquisition of Serra Verde, Brazil’s only commercial-scale rare earths operation in Goiás. Brazil, which holds about 21 million tonnes of rare-earth reserves (second only to China), is advancing legislation for a $2 billion guarantee fund and $5 billion in tax credits to anchor domestic processing and technology transfer. For miners and investors, multi‑year licensing delays, post‑Brumadinho environmental scrutiny and sovereignty debates over “preferential access” remain the key schedule and permitting risks.

Copper futures on Comex jumped 2.4% to a record $6.69/lb, widening the premium over LME contracts, which rose 1.6% to nearly $14,200/t, as traders priced in possible new US tariffs on refined copper imports. Supply risk is intensifying, with Gulf disruptions choking sulphur flows, threatening sulphuric acid availability for roughly one-fifth of global mined copper and potentially curbing up to 4.8 Mt of production if the Strait of Hormuz closes. Refined output is already reacting, with China’s April production down 3% and further declines expected, even as copper prices are up more than 10% year-to-date.

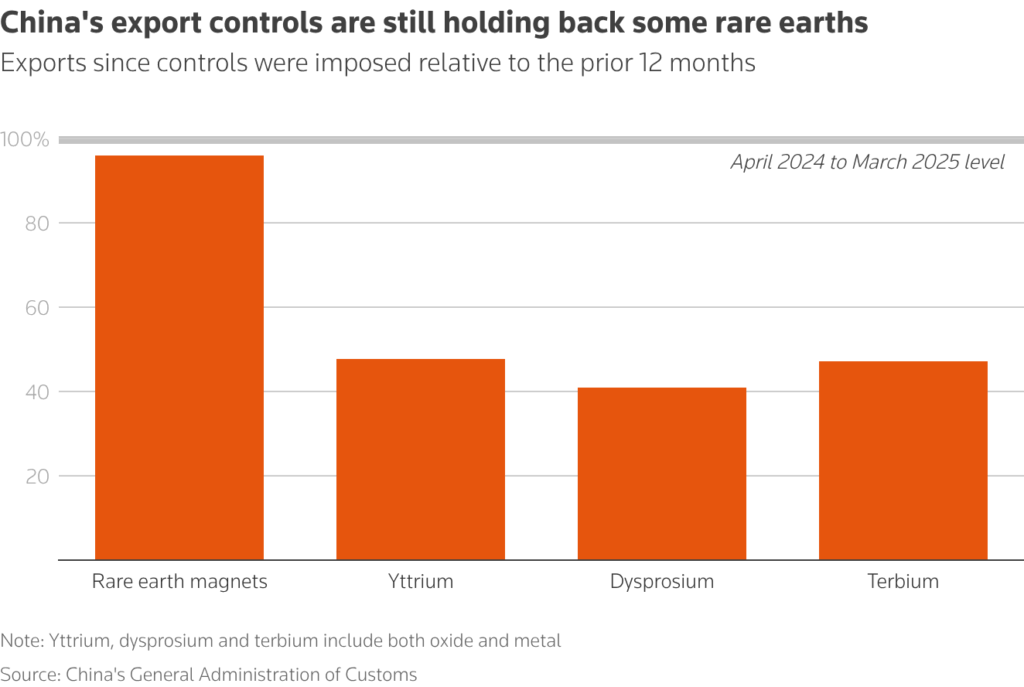

China’s April 2025 rare earth export controls remain in force despite Trump–Xi talks, with customs data showing exports of heavy rare earths yttrium, dysprosium and terbium still about 50% below pre-control levels. Prices outside China have surged, with dysprosium and terbium up four- to five-fold and yttrium reportedly about 140 times higher, while Japan has received only 4% of its former dysprosium volumes and Germany none. US aerospace manufacturers have already paused production due to yttrium shortages, and magnet buyers are paying 1.5–3 times more, signalling prolonged cost and supply risk for EV, wind and defence supply chains.

Agnico Eagle Mines will invest C$14 billion in Ontario by 2030, backed by the province’s new “One Project, One Process” permitting regime that targets approvals for advanced exploration and mine development within two years. About C$2 billion is earmarked for the Detour Lake underground expansion and the Upper Beaver gold-copper project, both >C$1 billion builds, adding up to 1,600 jobs and nearly C$5 billion to GDP. Detour Lake’s underground mine is designed to extend life to 2054, while Upper Beaver is planned as a 210,000 oz/y gold and 3,600 t/y copper operation over 14 years.

Titan Mining has signed a cooperation agreement with Teck Resources to assess recovering about 13,000 kg/year of germanium from existing process waste streams at the Empire State Mine zinc operation in New York, using Teck’s Trail Operations in British Columbia as the potential processing hub. The partners will test upgraded ESM process streams as germanium-bearing feedstock and negotiate volumes, payability and possible long-term offtake, targeting a capital-efficient flowsheet that avoids new mining. With US warehouse prices at US$5,800–8,600/kg and minimal domestic output, successful recovery could add significant incremental cash flow and establish Titan as a US germanium supplier.

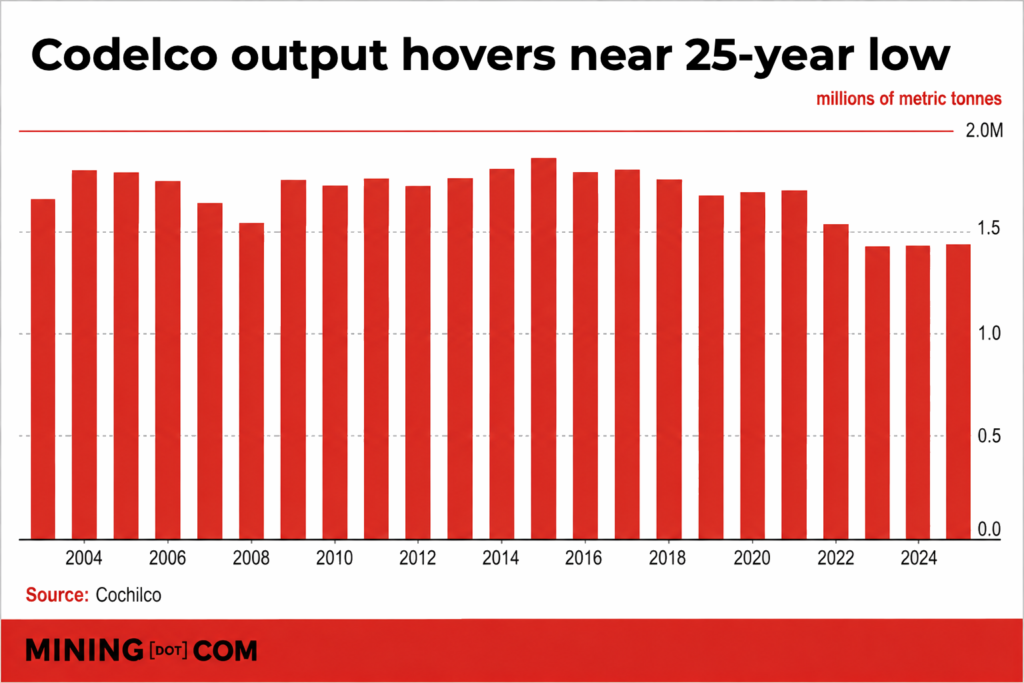

Codelco faces a preliminary internal audit finding that about 20,000 tonnes of material were wrongly counted as December 2025 finished copper, inflating reported output to 172,300 tonnes versus a January–November average of 105,600 tonnes. The disputed tonnage, allegedly authorised by a senior executive outside normal approval channels, comes amid Cochilco data showing January production slumping to 91,000 tonnes and March to 110,900 tonnes, raising doubts over any genuine recovery. Consultants Plusmining and GEM warn of serious governance, traceability and classification issues, with calls for an external audit and potential implications for executive incentives.

Amnesty International accuses Nevada’s three major lithium projects – Lithium Americas’ Thacker Pass, Ioneer’s Rhyolite Ridge and Surge Battery Metals’ Nevada North – of proceeding on ancestral lands without free, prior and informed consent, exposing a gap between US consultation-based permitting and UNDRIP standards. Ioneer cites 328 documented contacts with 13 Tribal Nations, voluntary cultural monitoring agreements and a Nevada District Court decision upholding its federal permit, while Lithium Americas plans US$1.3–1.6 billion capex for Thacker Pass Stage 1. Amnesty warns that advancing large, long-life assets such as Rhyolite Ridge, now scoped at 1.92 Mt LCE over 95 years with US$1.67 billion capex, without consent raises long-term reputational and regulatory risk.