China’s grip on rare earths: supply risk and cost signals for project teams

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

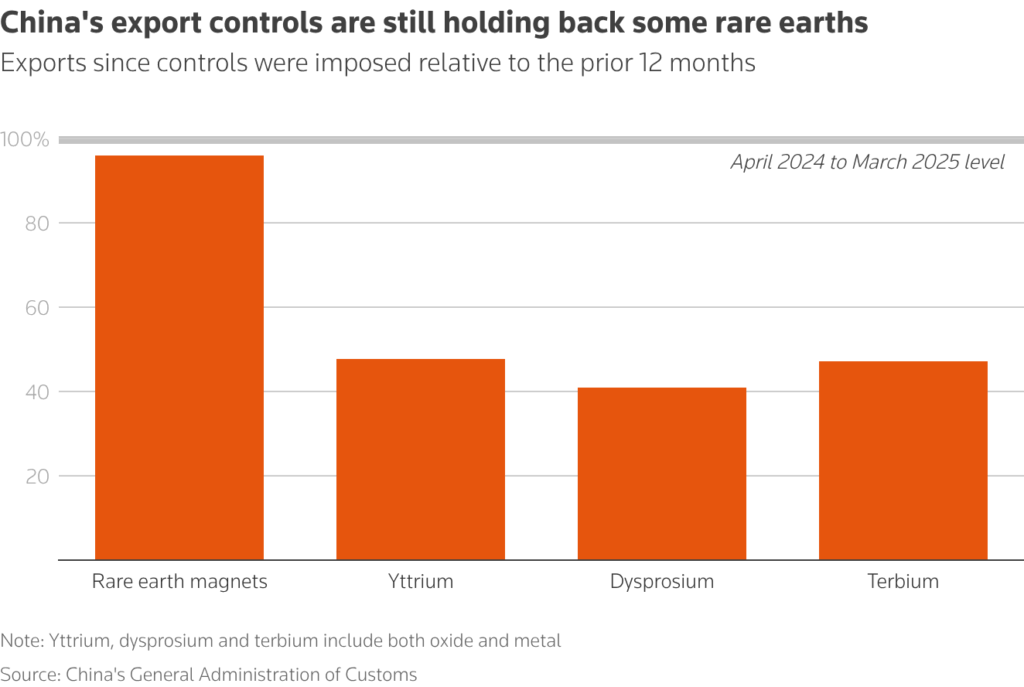

China’s April 2025 rare earth export controls remain in force despite Trump–Xi talks, with customs data showing exports of heavy rare earths yttrium, dysprosium and terbium still about 50% below pre-control levels. Prices outside China have surged, with dysprosium and terbium up four- to five-fold and yttrium reportedly about 140 times higher, while Japan has received only 4% of its former dysprosium volumes and Germany none. US aerospace manufacturers have already paused production due to yttrium shortages, and magnet buyers are paying 1.5–3 times more, signalling prolonged cost and supply risk for EV, wind and defence supply chains.

Technical Brief

- April 2025 export controls were imposed specifically in retaliation for Trump’s “Liberation Day” tariffs.

- Controls are administered via selective export licensing, targeting defence and advanced-technology supply chains per Arthur D. Little.

- White House claims from the October South Korea summit about “effectively eliminating” controls have not materialised.

- China’s Ministry of Commerce states export applications are still being approved for “eligible” buyers, implying case-by-case vetting.

- A major US industrial group reportedly lost hundreds of millions of dollars in monthly revenue before direct White House intervention.

- Several US aerospace manufacturers have already executed temporary production pauses directly linked to yttrium supply disruptions.

- Japan is identified as the largest rare earth magnet producer outside China, magnifying dysprosium supply risk for its downstream OEMs.

- Analysts such as Project Blue warn that non-Chinese mining, refining and magnet projects will take years to materially offset China’s leverage.

Our Take

In our database of 1176 Mining stories, rare earths pieces are still relatively few compared with bulk commodities, so a 140‑fold move in yttrium and four‑ to five‑fold spikes in dysprosium and terbium prices stand out as some of the sharpest price dislocations currently tracked.

The fact that Japan has received only 4% of its previous dysprosium import volumes from China suggests near‑term project finance for non‑Chinese rare earths and magnet materials in countries like Canada and the USA will likely find stronger policy and OEM backing than typical greenfield mining schemes.

Nouveau Monde Graphite’s presence alongside rare earths in this coverage underlines that graphite is increasingly being discussed in the same strategic breath as dysprosium and terbium, which in our database tends to coincide with downstream OEMs seeking multi-commodity offtake security rather than single‑metal deals.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.