Geomechanics, Streamlined.

© 2026 Geomechanics.io. All rights reserved.

Mandatory biodiversity net gain (BNG) for nationally significant infrastructure projects (NSIPs) has been pushed back to November 2026, a six‑month delay from the original May 2026 start. The deferral affects DCO‑consented schemes such as major highways, rail corridors and large energy projects, which will ultimately need to evidence at least 10% biodiversity uplift using habitat units and metric‑based baselines. Designers and environmental consultants gain extra time to refine baseline surveys, habitat creation plans and long‑term management obligations before BNG becomes a legal requirement.

Development consent has been granted for the 1.5GW Outer Dowsing offshore wind farm, to be constructed 54km off the Lincolnshire coast in the North Sea. The nationally significant infrastructure project will require extensive marine foundations, subsea cabling and grid connection works sized for utility-scale export of 1.5GW to the onshore network. Geotechnical and marine contractors can now progress detailed design for turbine foundations, seabed surveys and installation methodologies under the Development Consent Order framework.

A UK Government-commissioned feasibility assessment on building new nuclear power plants at existing Scottish nuclear sites is now unlikely to be released before the Scottish Parliament elections on 7 May. The study is expected to focus on brownfield nuclear locations such as Hunterston and Torness, assessing grid connection capacity, cooling water availability and regulatory constraints under Scotland’s current anti-nuclear policy. The delay leaves developers and consultants without key data on potential reactor siting, licensing timelines and supporting civil works for any future large-scale or SMR projects.

A Worcestershire vehicle maintenance firm has been fined £30,000 plus £4,325 in costs after a worker was crushed beneath a one-tonne concrete block, sustaining what the court described as “devastating” injuries. The incident involved a precast block used on the company’s site, with inadequate control of lifting and securing operations identified as the core failure. The case signals continued regulatory pressure on small depots and workshops to apply full CDM- and LOLER-level rigour to handling heavy concrete units and temporary yard structures.

Over 75% of residents in Aberdeen and Aberdeenshire back reopening the former rail links from Dyce to Ellon and onward to Peterhead and Fraserburgh, according to polling by the local chamber of commerce. The corridors, closed under Beeching-era cuts, would reconnect coastal towns of more than 30,000 people to the Aberdeen–Inverness main line, offering an alternative to the A90 and A952. For civil and rail engineers, the figures signal strong political cover for route safeguarding, new alignments around developed sections, and potential phased heavy rail or tram-train options.

Holcim UK is deploying 20 LiuGong 870HE pure electric wheel loaders across its quarry fleet, expanding one of the highest-tonnage battery-electric loader deployments in the sector. The 870HE units, among the largest pure electric loaders currently available, are targeted at high-duty quarry loading cycles traditionally dominated by diesel machines. For geotechnical and quarry operators, this signals accelerating adoption of heavy battery-electric equipment for primary load-and-haul, with implications for power supply design, charging infrastructure layout and ventilation requirements in future pit and plant planning.

Critical Metals Corp’s share price jumped 23.6% in pre-market trading to $11.46, valuing the company at $1.4 billion, after Greenland approved the indirect transfer of the Tanbreez rare earth mining licence, allowing Critical Metals to move to a 92.5% stake, with European Lithium retaining 7.5%. The Tanbreez deposit at Killavaat Alannguat hosts a 45-million-tonne resource grading 0.40% total rare earth oxides, with 27% heavy rare earths (Dy, Tb, Y), and a March 2025 PEA valued the project at about $3 billion. A phased plan targets initial output of ~85,000 tonnes of rare earth oxides per year, scalable to 425,000 tonnes, backed by a 10-year offtake to Ucore’s Louisiana plant, a Qaqortoq pilot facility, and eligibility for up to $120 million in US EXIM financing.

Aluminum Corp of China is deploying over $700 million in the next three years at the 4,500-metre-high Toromocho open-pit in Junín to lift concentrator capacity from 117,000 to 170,000 tonnes per day and add molybdenum recovery via a new ore classification system. The staged $1.7 billion programme includes a $1.35 billion plant expansion plus about $350 million of technical modifications, expanded low-grade stockpiles inside and west of the pit, and autonomous drilling and fleet management developed with Huawei Peru. Toromocho currently produces about 250,000 tonnes of copper concentrate annually, accounts for roughly 10% of Peru’s copper output, and is expected to run to 2042 amid rising political risk over unused concessions.

Exploration and evaluation spending in British Columbia hit a record C$751 million in 2025, up 36% year-on-year, even as other major provinces such as Ontario and Quebec saw exploration budgets fall. Copper became BC’s top exploration target for the first time, attracting C$384 million—just over half of total spend—driven by large porphyry systems in the Golden Triangle and projects such as Galore Creek and Eskay Creek. Juniors led the rebound, lifting their outlay 47% to C$479 million on improved financing and expanded grassroots drilling and geophysics.

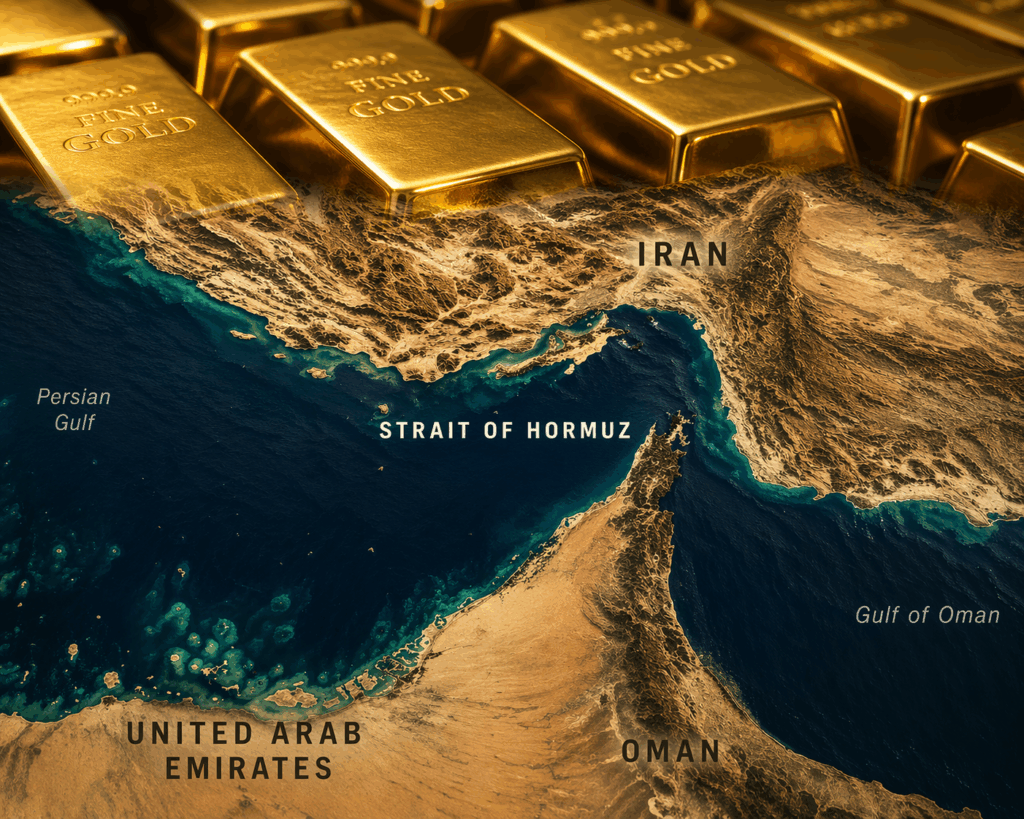

Gold jumped 1.7% to about $4,887/oz, its highest level since 17 March, after Iran reopened the Strait of Hormuz, restoring commercial traffic through a corridor that carries roughly 20% of global oil flows. Silver climbed more than 5% to $83/oz, a five-week high, as easing energy-price and inflation fears revived expectations of interest rate cuts that favour non-yielding assets. Analysts at Zaner Metals and MKS PAMP see scope for a move back towards $5,000/oz in the near term, while Goldman Sachs keeps a bullish $5,400/oz year-end target.

USA Rare Earth has produced its first commercial pour of 2N–2N5 purity (99%–99.5%) yttrium metal via subsidiary Less Common Metals at its Cheshire, UK facility, joining the small group of non-Chinese commercial yttrium suppliers after 2025 prices spiked about 1,500% on Chinese export curbs. The output underpins USAR’s mine-to-magnet plan anchored by the Round Top rare earth deposit in Texas, targeted for 2028 production, and a newly commissioned sintered neodymium magnet line in Stillwater, Oklahoma, with a potential second magnet plant in France. Backed by a US$1.58 billion Trump administration investment for an 8%–16% equity stake, USAR is positioning to supply aerospace, defence and advanced ceramics users seeking alternatives to Chinese yttrium.

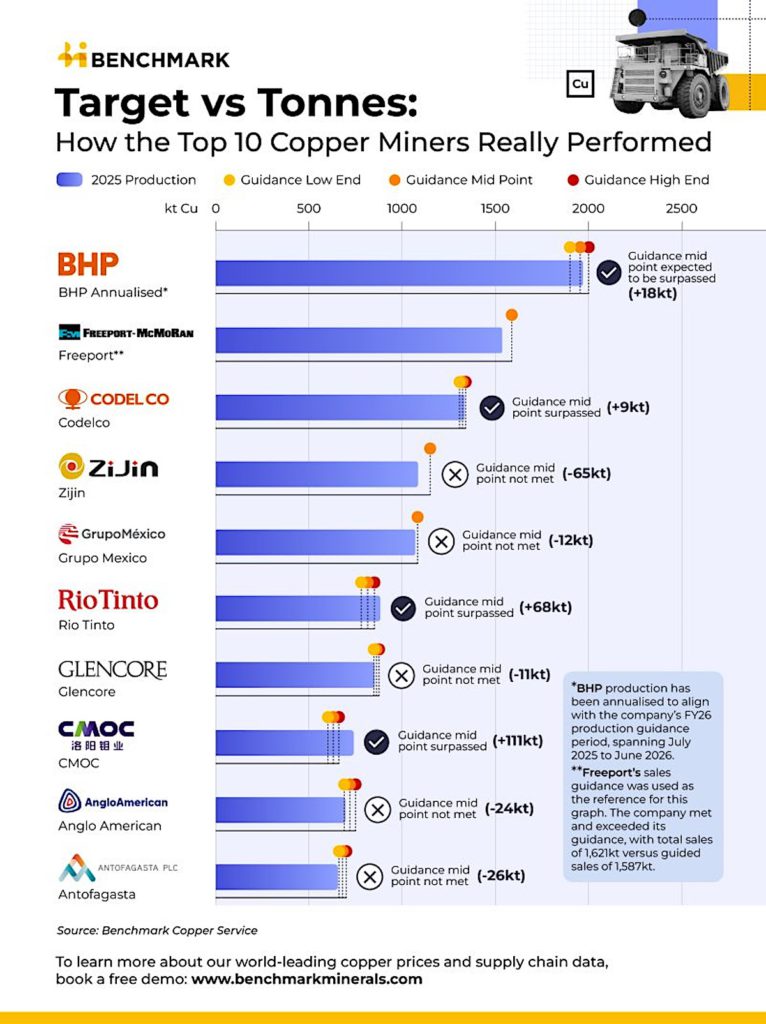

Benchmark Mineral Intelligence reports that 2025 copper production deviated sharply from company guidance, with CMOC beating its target by 111,000 tonnes while Zijin Mining missed by 65,000 tonnes due to delays at the Julong expansion and weaker African output. The analysis explicitly separates stated guidance from realised tonnages, showing that most copper supply models still treat guidance as production. For mine planners and market modellers, the data signal that project delays and operational volatility can materially distort supply curves if guidance is used unadjusted.

Fast-tracking US critical minerals projects under President Trump’s March 2025 executive order has seen some mining permits issued in as little as 20 days, prompting Oxfam America to warn that compressed timelines without robust environmental review and community consultation could trigger force majeure events, legal challenges and multimillion-dollar delays. Oxfam policy leads Emily Greenspan and Andrew Bogrand argue that IFC performance standards should be treated as a minimum and that US-backed export credit and development finance should be tied to IRMA’s more stringent audit regime. They also caution that the industry-led Consolidated Mining Standard Initiative could dilute existing benchmarks and that policymakers still underestimate the globalised nature of refining and processing, particularly in regions such as Africa’s Copperbelt.

The Metals Company’s NORI and TOML subsidiaries have submitted 2013–2022 exploration data from the eastern Clarion‑Clipperton Zone to the ISA’s DeepData system, including 777 equipment deployments, over 4,800 environmental samples, 76,000 biological records and 69,185 geochemical data points from depths beyond 4,000 m. The dataset now accounts for roughly one‑third of all CCZ entries in DeepData and 54% of biological records in the OBIS‑ISA node, positioning it as a key reference for Environmental Impact Assessments. TMC argues this evidence base is sufficient to start monitored commercial nodule collection, despite ongoing calls from NGOs for a moratorium.

Oxford University spinout Ascension has raised £1.7 million in new funding, combining a £670,490 Innovate UK Growth Catalyst grant with £1 million from UKI2S, Oxford Science Enterprises and East X, bringing total capital raised to £6.2 million. The company’s Selective Recovery programme targets rare earths and other critical minerals in deep volcanic glass, aiming to separate metals in situ and cut surface processing stages. Ascension’s process uses natural geothermal heat in volcanic rock deposits, avoiding excavation, high-temperature surface processing and associated land disturbance.

MMD Group has signed a Memorandum of Agreement with CiDi Inc. to embed CiDi’s autonomous driving technology into MMD’s TraxIQ material handling platform, adding driverless capability to its existing digital haulage management. MMD will retain responsibility for global commercialisation and deployment of TraxIQ, while CiDi supplies the autonomy stack, sensors and control software for mobile equipment operating within the system. The move signals further integration of fleet autonomy with real-time material tracking, dispatch and crusher-feed optimisation in brownfield and greenfield haulage circuits.

Australia’s asphalt sector, led by guidance from the Australian Flexible Pavements Association (AfPA) and Projects Technical Advisor Trevor Distin, is pushing performance-based mix design to exploit asphalt’s 100 per cent recyclability and cut pavement carbon. Reclaimed asphalt pavement (RAP) is being reprocessed into new surface and base courses, with higher RAP contents enabled by rejuvenators, tighter binder grading and improved plant controls. For designers and asset owners, the shift means specifying functional performance (rutting, fatigue, texture, skid resistance) and lifecycle cost rather than prescriptive mix recipes.

LiuGong’s 856T wheel loader has been selected by Australian Sandstone Merchants in New South Wales as the primary machine for high-duty quarry operations, handling dense sandstone blocks and continuous loading cycles. The 856T, part of LiuGong’s long-running wheel loader line dating back to 1958, is being used for both face loading and stockpile management, where breakout force and stability on uneven quarry floors are critical. For operators, the choice signals growing confidence in Chinese-built loaders for heavy quarry applications traditionally dominated by established Western brands.

Wirtgen has launched its next-generation WR series stabilisers, led by the WR 240 X, for cold recycling and in-situ pavement stabilisation across Australian road projects. The machines build on the previous WR range with higher fuel-efficiency, integrated operator assistance systems and smarter process control for mixing, water and binder dosing. For geotechnical and pavement engineers, the focus is on more consistent subgrade and basecourse treatment in a single pass, improving layer uniformity and shortening construction windows on rehabilitation jobs.

AIC Mines reported strong March quarter 2026 growth driven by the Eloise copper mine, where successful drilling extended high-grade mineralisation and a process plant expansion lifted nameplate throughput. The upgraded concentrator, incorporating additional grinding capacity and upgraded flotation cells, is targeting higher copper recovery and lower unit costs as ore feed ramps up. For engineers, the key watchpoints are how the expanded plant handles variable underground ore characteristics and whether further debottlenecking of crushing and tailings infrastructure will be required as throughput approaches design limits.

Catalyst Metals is advancing towards first gold production from the Trident underground mine at Plutonic after reporting strong grade control drilling results that confirm continuity of high-grade lodes. The work forms part of Catalyst’s broader Plutonic gold strategy in Western Australia, where detailed grade control is being used to refine stope designs and de-risk early mining panels. For geotechs and mine planners, the results support tighter reconciliation, more confident ore–waste boundaries and potentially improved scheduling for initial stoping blocks.

Rising global defence spending on missiles, drones and advanced electronics is sharply increasing demand for critical minerals such as rare earths, high‑purity aluminium, titanium, nickel and specialised battery metals. Modern defence platforms now embed complex materials across guidance systems, radar, propulsion and armour, tightening specifications on purity, magnetic behaviour and high‑temperature performance. For miners and processors, this points to long‑term offtake potential for Australian rare earths, titanium and nickel projects, but also stricter ESG, traceability and supply‑security requirements in defence‑linked supply chains.

Newmont is steadily ramping up processing operations at the Cadia gold mine in New South Wales after a magnitude-4.5 earthquake on Tuesday, with inspections so far indicating no material impact to underground workings or surface infrastructure. Geotechnical and structural assessments are ongoing across key assets including the tailings storage facilities, process plant foundations and underground openings. The event will interest operators of deep and seismically sensitive mines reviewing ground support design, real-time seismic monitoring and business-continuity planning for moderate local seismicity.

Exploration activity is ramping up across Australia, with Rincon Resources expanding gold–copper targets at its Telfer South project, Hillgrove Resources progressing work at the Kanmantoo copper mine, and Auravelle Metals advancing its battery metals portfolio. Rincon is extending drilling and geophysics south of Newcrest’s Telfer operations, targeting deeper intrusive-related mineralisation, while Hillgrove focuses on resource growth and underground potential at the existing open pit. For geotechs and mine planners, the work signals more near-mine drilling, deeper targets and potential future cutbacks or underground access designs.