Geomechanics, Streamlined.

© 2026 Geomechanics.io. All rights reserved.

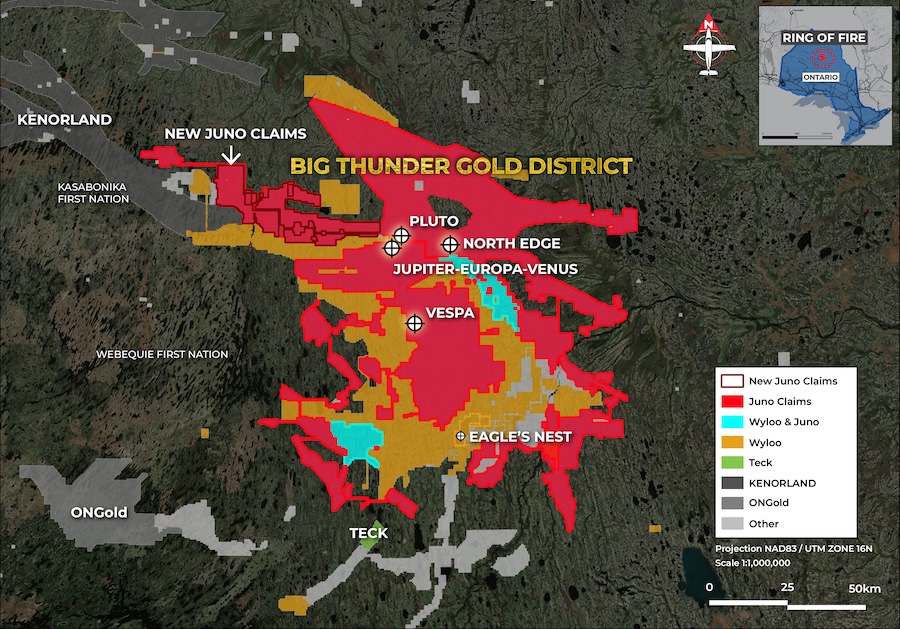

Juno Corp, led by founder and CEO Robert Cudney, is launching the largest exploration programme in more than a decade in Ontario’s Ring of Fire, controlling 29,956 claims over roughly 5,796 km²—just over half the camp—and anchored by the high‑grade Jupiter copper‑zinc‑silver VMS deposit. Cudney is renaming Northfield Capital as Juno International and has secured logistics by acquiring Sudbury-based True North Airways, while the company’s Big Thunder grassroots gold find has already earned the 2026 Bernie Schnieders Discovery of the Year Award. Veteran geologist John Harvey compares the camp’s long‑term potential to, and possibly exceeding, the Sudbury Basin and South Africa’s Bushveld Complex.

Iamgold has lifted contained gold at the Côté mine in northeastern Ontario by 12% to 20.34 million oz., integrating the Gosselin zone into a combined resource of 838 million tonnes at 0.75 g/t and inferred resources of 177.1 million tonnes at 0.61 g/t for 3.48 million oz. The update uses a higher gold price assumption of US$2,500/oz and a lower cut-off grade of 0.25 g/t, and underpins a planned 40% plant expansion to more than 50,000 tonnes per day. A new technical report due by year-end will address reserve conversion, strip ratio, tailings and processing rates, while 30,000 metres of additional diamond drilling is scheduled for 2026 to refine the Côté-Gosselin model and test district targets such as Jerome, Northshore and Monella Point.

Cameco has agreed to pay C$115.75 million to acquire TEPCO Resources’ 2.871% stake in the Cigar Lake uranium joint venture, lifting its ownership in the northern Saskatchewan mine to 57.418% while Orano’s share rises to 42.582%. Cigar Lake, about 660 km north of Saskatoon, has produced 174.5 million lb of U3O8 since 2014 and still holds 172.4 million lb in reserves plus 46.3 million lb in combined resources. Cameco forecasts 2026 output at 17.5–18 million lb U3O8 (100% basis) and is targeting mine life extension to 2036.

Gold prices fell nearly 2% on Monday, with spot gold hitting a weekly low of about $4,450/oz and three‑month New York futures holding just above $4,500/oz, as renewed US strikes on Iranian military sites pushed oil and the dollar higher. Traders now assign roughly a 39% probability to a 25‑basis‑point Federal Reserve rate hike in December, according to CME FedWatch, dampening appetite for non‑yielding bullion. Despite the pullback from January’s record near $5,600/oz, JPMorgan and Goldman Sachs still project average 2026 prices of $5,000/oz and $5,400/oz respectively.

Barrick is considering carving out its African mines into a London‑listed vehicle via a potential $30 billion combination with Endeavour Mining, while retaining a Toronto holding company for its New York‑listed shares. The move would mirror Barrick’s earlier Acacia spin‑off and comes as it plans a separate New York listing for its Nevada and Dominican Republic assets by end‑2026, shifting capital towards lower‑risk jurisdictions. A tie‑up would pool Barrick’s Kibali, North Mara, Bulyanhulu, Lumwana and Tongon operations with Endeavour’s West African portfolio, currently targeting about 1.2 million oz of gold output this year.

Activist fund Elliott Investment Management has confirmed a roughly A$1 billion stake in Northern Star Resources, giving it about 4% of the ASX-listed gold producer and placing it among the top five shareholders alongside Van Eck and BlackRock. Elliott is pushing for a new mining-experienced board, an external CEO and a formal strategic review, citing “repeated operational missteps”, cost overruns and “deeply inadequate disclosures” at assets including the KCGM open pit in Kalgoorlie. The move follows two production downgrades in 2026, supply issues at KCGM and a share price fall of up to 30% this year despite strong gold prices.

Orla Mining has halted all operations at its Camino Rojo open-pit gold mine in Zacatecas, Mexico, after unionised workers launched a blockade over a productivity bonus and statutory profit-sharing payments, knocking TSX-listed shares down 7.5%. The mine produced 96,764 oz of gold in 2025 and was guided to deliver 110,000–120,000 oz in 2026 at all-in sustaining costs of $1,150–$1,250/oz, making any prolonged stoppage material for mine planning and contractor utilisation. The disruption also injects risk into Orla’s planned all-stock $18.5 billion merger with Equinox Gold, which targets combined output of about 1.1 Moz/year.

Americas Gold and Silver’s latest Cosalá infill drilling at the San Rafael Upper and 120 zones is returning silver grades up to five times above the current resource model, including 14 metres at 599.8 g/t Ag and 0.83% Cu from 38.2 metres and 45 metres at 342.9 g/t Ag and 0.85% Cu from 106 metres, feeding directly into H2 mine plans. At Idaho’s Galena Complex, narrow-vein hits such as 0.21 metre at 24,913 g/t Ag and 16.9% Cu on the 149 Vein and new 43L-TJ vein mineralisation sit close to existing infrastructure. The company is backing a 64,000‑metre, US$20 million drilling campaign with processing upgrades including a paste backfill plant, No. 3 shaft hoist to ~105 short tons/hour and a mill expansion from 750 to 1,200 tons/day, supporting guidance of 3.2–3.6 Moz Ag in 2026.

Ramaco Resources has signed a non-binding MoU with REalloys Inc. to supply mixed rare earth carbonate from the Brook mine in Wyoming, described as the USA’s largest unconventional rare earth and critical mineral deposit hosted in coal and carbonaceous ore. REalloys will separate Ramaco’s MREC into individual oxides at the Saskatchewan Research Council facility in Canada, while Ramaco will also provide separated scandium oxide for alloy metallisation at REalloys’ Euclid, Ohio plant. A 2025 preliminary economic assessment for Brook reported a post-tax NPV of about $1.2 billion, 38% IRR and initial capex of $473 million.

Sandvik has partnered with Rio Tinto to integrate an autonomous drilling system (ADS) with Sandvik surface drill rigs, combining Rio Tinto’s remote operations experience with Sandvik’s AutoMine automation platform. Development will start at Sandvik’s Finnish facilities, then shift to Rio Tinto’s Perth operations centre for field trials across multiple rigs and sites. The work targets interoperable, mixed‑model autonomous drill fleets for large open‑pit mines, signalling future requirements for common control platforms and remote supervision of distributed drilling operations.

BHP is advancing renewable electricity self-supply and storage at its Escondida and Spence copper mines in Chile through new long-term agreements with Sungrow to keep both operations on 100% renewable power. The deals cover large-scale solar generation and battery energy storage systems sized to support long-term production growth and process stability at high-altitude, grid-constrained sites. For mine planners and process engineers, firmed renewable supply reduces exposure to grid curtailment and power price volatility while tightening decarbonisation baselines for future brownfield expansions.

Minera Las Bambas SA, part of MMG, has ordered a major new Caterpillar fleet from Peruvian dealer Ferreyros, with scope to expand to 45 units, anchored by 27 Cat 798 ultra-class trucks rated at 400 t payload. Ferreyros is scheduled to deliver more than 20 machines in 2026, signalling a substantial ramp-up in high-capacity haulage at the Las Bambas copper operation in Apurímac. The deal points to continued preference for ultra-class diesel haulage over trolley or autonomous solutions at this high-altitude open pit.

ESG technology is reshaping Australian mine design and operations by embedding real-time environmental, social and governance data into planning, approvals and day‑to‑day control. Operators are deploying integrated ESG platforms that pull live inputs from dust and noise monitors, water‑quality sensors and energy‑metering systems to automate compliance reporting and adjust haulage, dewatering and ventilation schedules. For geotechs and mine planners, this means designs increasingly need to accommodate dense sensor networks, verifiable rehabilitation metrics and auditable ESG baselines from feasibility through closure.

Cornwall Council has approved a feasibility study into reinstating a through rail link between Okehampton and Penzance, potentially creating an additional inland corridor to the existing Dawlish coastal route. Engineers will examine track capacity, alignment constraints on legacy formations, and options for upgrading structures, level crossings and signalling to modern standards. For civil and geotechnical teams, the work will focus on earthwork stability on steep Cornish and Devon cuttings, flood‑prone sections, and interfaces with existing main line operations.

Major UK contractors and consultants have reshuffled senior leadership in May 2026, with several firms creating new roles focused on complex infrastructure delivery and digital project controls. Key moves include board-level changes on multi‑billion‑pound rail and highway frameworks and new directors appointed to oversee NEC4 contract management and BIM‑enabled design for large bridges and tunnels. For geotechnical and civils teams, the changes signal fresh decision‑makers on ground risk allocation, value engineering of foundations and retaining structures, and adoption of data‑driven asset management.

Surging UK industrial energy prices are eroding manufacturers’ margins by consuming a larger share of operating budgets and constraining capital for plant upgrades. A new report urges factories to prioritise energy-efficient motors, variable-speed drives on pumps and fans, and improved process heat recovery to cut electricity and gas demand. For civil and building engineers designing or refurbishing manufacturing facilities, the message is to integrate high-efficiency services, sub-metering, and better building fabric performance early to protect long-term competitiveness.

WSP has secured supplier status on all three Flood Risk and Asset Management (FRAM) lots under the UK Government Commercial Agency’s Construction Professional Services 2 (CPS2) framework, covering strategic flood risk assessment, asset management and related design services. The “significant multi-year” framework will channel central government and agency commissions for flood modelling, defence appraisal and lifecycle planning of existing assets. For consultants and contractors, CPS2 FRAM awards signal sustained demand for integrated hydraulic modelling, geotechnical assessment of embankments and structures, and data-led asset condition monitoring.

Saudi Arabia’s Neom gigaproject, which bundles five megaprojects including the 170km-long linear city The Line, appears to have stalled completely, according to a public relations professional who previously represented the scheme. The reported pause raises fresh uncertainty over large-scale enabling works, including desert earthworks, coastal reclamation and deep foundation packages already tendered or partially mobilised. Contractors and consultants with exposure to Neom’s early-stage infrastructure may now face demobilisation, contract renegotiation and delayed cashflow on geotechnical investigations, transport corridors and utilities corridors planned for the site.

Sweco has secured a £11M framework agreement with the Norwegian Water Resources and Energy Directorate (NVE) to deliver consulting services for flood and erosion protection schemes across Norway. The multi-year framework will cover planning and design of river training works, bank stabilisation and flood defences, including hydraulic modelling and geotechnical assessments for vulnerable catchments. For UK and European consultants, the deal signals continued demand for specialist expertise in climate-resilient infrastructure, particularly in steep, glacially influenced valleys and high-flow Nordic river systems.

The process to fully review HS2 exposes systemic weaknesses in UK megaproject delivery, echoing historic issues on schemes such as Crossrail and the Channel Tunnel where scope creep, under-estimated ground risk and optimistic demand forecasts drove major cost overruns. Comparisons focus on early-stage geotechnical investigation density, contingency levels for complex tunnelling and viaduct works, and governance structures separating client, designer and delivery partners. For current and future high-speed rail and large civils projects, the message is tighter risk quantification, more conservative programme allowances and clearer accountability for interfaces and design changes.

AtkinsRéalis has secured a multi‑year professional services framework with EDF to support construction of the 3.2GW Sizewell C nuclear power station in Suffolk, continuing its role from the Hinkley Point C programme. The framework is expected to cover civil, structural and geotechnical design, digital engineering and site-based technical support across major assets such as the nuclear island, conventional island and marine works. For practitioners, the deal signals long‑term demand for nuclear-grade concrete, complex deep foundations and coastal protection design aligned with UK EPR requirements.

A 2‑day heavy-lift operation at Hinkley Point C has installed the second nuclear reactor using “Big Carl”, the world’s largest land-based crane. The lift involved precision placement of the reactor vessel into the reinforced concrete containment structure, integrating with pre-installed civil works and embedded systems. The operation confirms the site’s ability to execute ultra-heavy modular lifts, reducing on-site assembly time and driving tighter tolerances for future nuclear civil engineering packages.

Structured service level agreements (SLAs) from conveyor specialist Tru-Trac are shifting mine operators from reactive belt repairs to continuous performance optimisation on high‑tonnage lines. Instead of ad hoc call‑outs, Tru-Trac ties services such as belt tracking audits, idler and pulley inspections, and condition‑based replacement of critical components to defined uptime, spillage and mistracking thresholds. For geotechnical and plant engineers, this formalises conveyor availability as a design and operational parameter, directly affecting stockpile feed stability, crusher utilisation and overall materials handling throughput.

South Africa’s mining sector is being urged by Chris Campbell, CEO of Consulting Engineers South Africa (CESA), to move beyond the traditional pit-to-port model of exporting largely unprocessed ore towards domestic beneficiation and value-adding plants. Campbell calls for engineering-led investment in concentrators, smelters and refineries tied to existing iron ore, manganese, PGMs and battery mineral operations, supported by reliable 132–400 kV power, bulk water supply and upgraded rail sidings. The shift would require integrated mine-to-metals project planning, retooled EPCM contracts and stronger collaboration between miners, state utilities and local OEMs.