Top 20 automakers by battery metals spending: cost signals for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

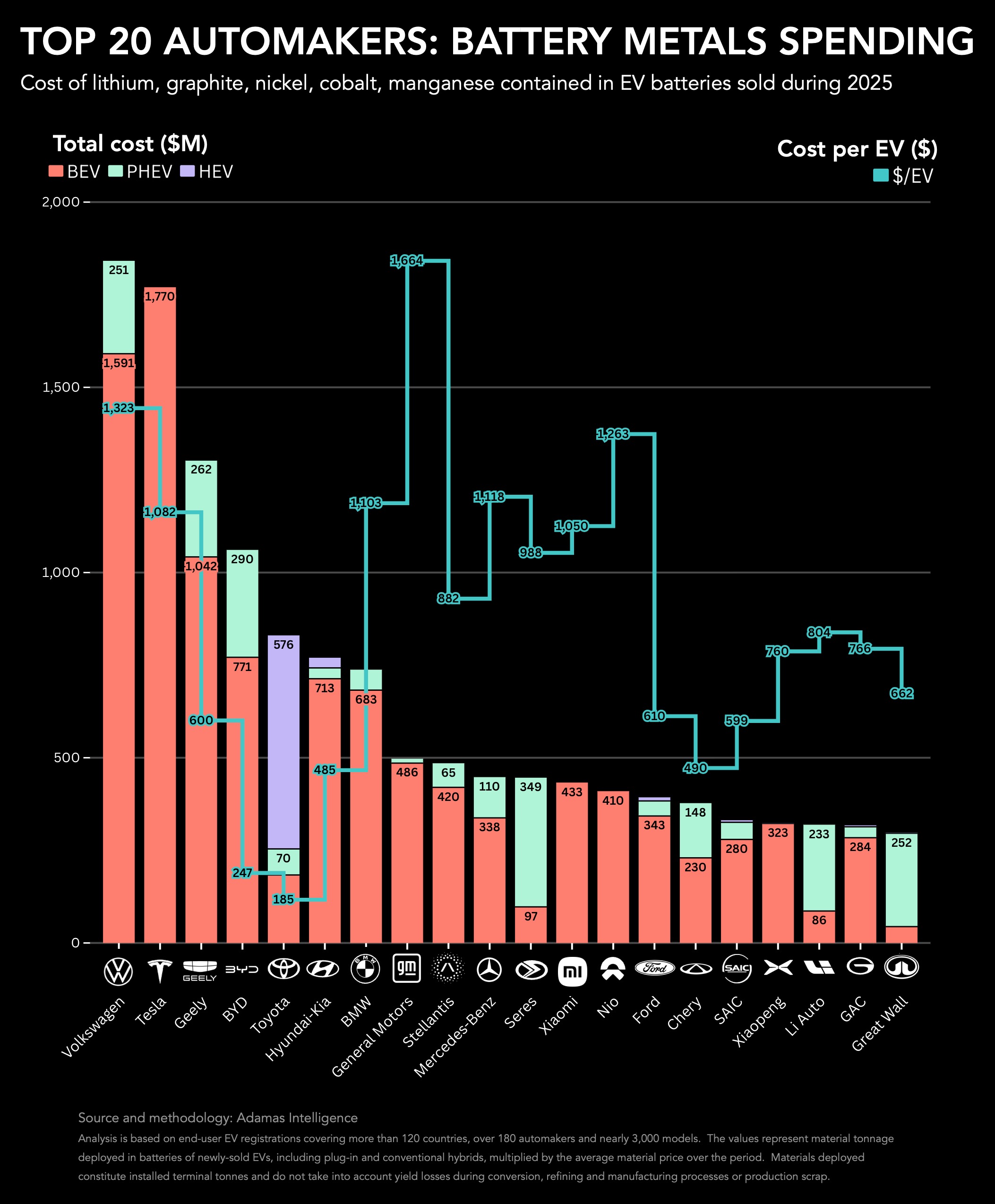

Global EV battery capacity deployment passed 1 TWh in 2025, nearly quadruple 2021 levels, yet the raw material bill for lithium, graphite, nickel, cobalt and manganese in passenger EVs reached only $15.6 billion, still about half the 2022 peak. BYD’s all‑LFP, lower‑end line-up and heavy plug‑in hybrid mix kept average battery metals spend to $247 per EV (US$366 per BEV), versus Tesla’s US$1,082 and Volkswagen’s US$1,624 per BEV, with VW now the largest battery metals spender. GM’s NCMA‑heavy Ultium strategy yields an average US$1,664 per EV and is being retooled towards LFP, while Toyota’s HEV‑dominated portfolio limits spend to US$185 per vehicle.

Technical Brief

- EV battery capacity deployment exceeded 1 TWh in 2025, up from 286 GWh in 2021.

- Global passenger EV (including HEV, PHEV, BEV) sales approached but did not reach 30 million units.

- Year-on-year, passenger EV unit sales grew 18%, while deployed battery capacity grew 22%.

- Market size in GWh is now roughly 10 times larger than in 2019.

- Raw material spend on lithium, graphite, nickel, cobalt and manganese reached US$15.6 billion in 2025, up 11%.

- That US$15.6 billion excludes processing, conversion and scrap losses, where yield losses can exceed 10–20%.

- LFP chemistries supplied nearly 50% of global deployed battery capacity, but hold ~70% share inside China.

- Outside China, high‑nickel NCM (>60%, often ≥80% Ni) remains the dominant cathode choice.

Our Take

BYD’s low average material cost per EV and heavy use of LFP chemistry aligns with its parallel push into stationary storage and mining haulage batteries, as seen in our coverage of Fortescue’s 250 MWh BYD system in the Pilbara and BYD’s stake in Boonray’s autonomous mining trucks, signalling a vertically integrated play across both on-road and off-road electrification demand for lithium, iron and phosphate.

In our database of 1121 Mining stories and 120 battery-metals pieces, Tesla, BYD, Volkswagen and GM now dominate the demand-side narrative, which effectively shifts price and supply risk for lithium, nickel, cobalt and manganese from traditional OEMs to a smaller group of automakers with direct leverage over upstream offtake terms.

Toyota’s relatively low battery metals spend per EV, combined with a fleet still dominated by HEVs with sub-2 kWh packs, suggests that miners targeting higher-intensity BEV demand for nickel and cobalt will be more exposed to procurement strategies of BYD, Tesla and GM than to Japanese hybrid-heavy producers in the near term.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.