Met coal pipeline grows despite demand slide: project and ESG signals for mine teams

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

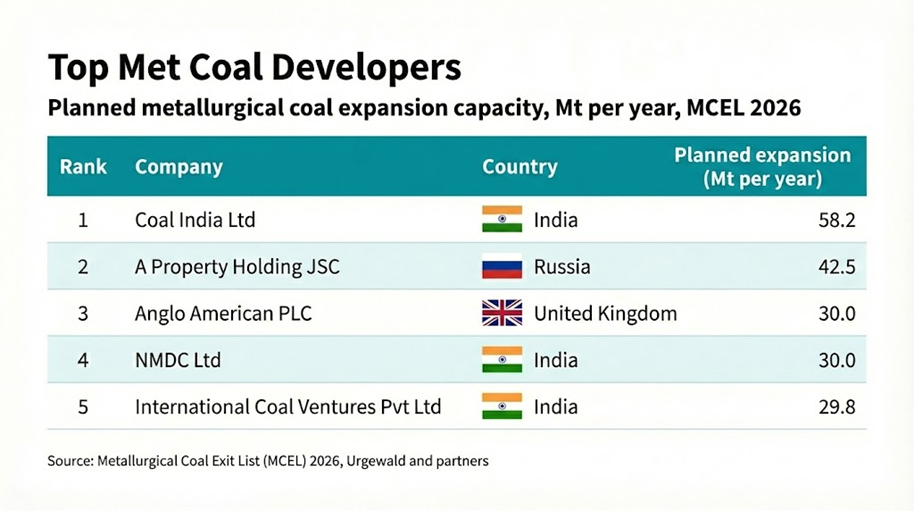

A new assessment by German NGO Urgewald finds 273 metallurgical coal projects planned or under construction across more than 20 countries, adding up to about 580 Mtpa of potential new capacity this decade, despite IEA forecasts of demand slipping from 1,114 Mt to 1,061 Mt by 2030. Australia leads the pipeline, with Queensland’s Moranbah South in the Bowen Basin flagged as the largest proposed pure met coal mine at 18 Mtpa, even as BHP drops the Saraji East expansion and Whitehaven shelves Blackwater North. Urgewald links the buildout to environmental impacts such as selenium contamination in Elk Valley, British Columbia, and notes over 150 financial institutions now use its Metallurgical Coal Exit List, with investors like Ilmarinen moving to divest from met coal developers.

Technical Brief

- Urgewald’s 2026 Metallurgical Coal Exit List tracks 145 parent companies plus 200+ subsidiaries in met coal.

- The report counts 273 mine projects (greenfield and expansions) across 20+ countries in various development stages.

- Queensland is identified as the main hub for new open-cut metallurgical coal proposals in Australia.

- BHP has cancelled the Saraji East expansion in central Queensland after earlier signalling met coal job cuts.

- Whitehaven has paused the approved Blackwater North project but continues advancing Blackwater South in the same region.

- Smaller met-coal-focused firms such as Coronado Global Resources and Bowen Coking Coal face pressure from weaker prices and higher royalties.

Our Take

A potential 52% increase in metallurgical coal capacity this decade, against an International Energy Agency-flagged demand drop, implies that higher-cost projects in Queensland’s Bowen Basin and Canada’s Elk Valley are likely to face margin pressure first if prices soften.

The 580 Mt/y of prospective met coal capacity in more than 20 countries in our database sits alongside a growing cluster of ‘Sustainability’-tagged steel decarbonisation pieces, signalling that financiers backing projects like Moranbah South or Castle Mountain will increasingly be benchmarked against alternative low-CO2 steel routes rather than thermal coal peers.

With over 150 financial institutions reportedly using the MCEL framework while US$52 billion has still flowed into met coal since 2022, operators such as BHP, Anglo American and Glencore are likely to encounter more fragmented capital markets, where European lenders tighten exposure even as some Asian and North American banks remain active for steel-linked coal assets.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.