Critical minerals diplomacy surge: project finance and offtake gaps for engineers

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

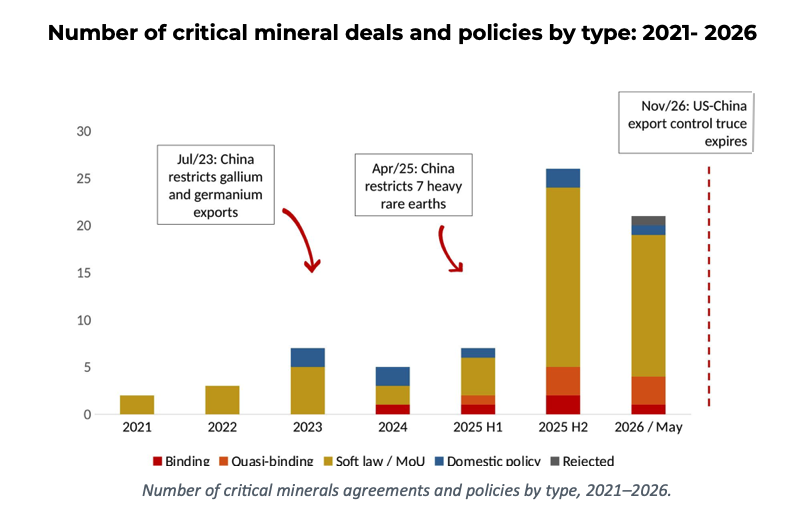

More than 70 critical minerals agreements have been signed since 2021, but over 60% are non‑binding frameworks without concrete investment, production, procurement or financing commitments, leaving China’s 60–90% control of rare earths refining and other midstream capacity largely unchallenged. The US has inked over 20 deals in 18 months and launched initiatives such as FORGE and the US‑EU‑Japan framework, yet only a handful are legally binding, creating a gap between diplomatic ambition and bankable project support. Africa, despite holding over 60% of global cobalt reserves, features in relatively few agreements, with contrasting cases such as a binding US‑DRC cobalt deal and Zambia’s rejection of proposed US conditions signalling producer countries’ growing leverage to demand local processing, infrastructure and policy flexibility.

Technical Brief

- More than 50 bilateral/multilateral critical minerals agreements have been announced in just the last 18 months.

- Over 60% of all post‑2021 critical minerals instruments are explicitly labelled as non‑binding MOUs, partnerships or cooperation frameworks.

- China retains an estimated 60–90% share of global rare earths refining capacity, anchoring midstream dominance.

- Agreements that embed price floors, stockpiling mechanisms, co‑financing, permitting cooperation or procurement support are flagged as most investment‑relevant.

- Non‑binding frameworks are noted as weak tools for securing offtake, public financing or protection from future policy reversals.

- Africa holds 60%+ of global cobalt reserves yet appears in only a small fraction of signed agreements.

- Binding deals are concentrated among a narrow group: Australia, Japan, Argentina, Ukraine and the Democratic Republic of Congo.

- The EU’s Critical Raw Materials Act is singled out as one of few frameworks with legally enforceable diversification requirements.

- Scheduled expiry of the current US‑China export‑control “truce” later this year is a key timing risk for supply‑chain planning.

Our Take

Plusmining’s role in this diplomacy piece echoes its appearance in our copper and lithium pricing coverage, signalling that its datasets are increasingly shaping how policymakers frame long-term assumptions for copper, cobalt and other critical minerals rather than just project financiers.

With Africa hosting about 60% of global cobalt reserves and China controlling an estimated 60–90% of rare earth refining, the lack of ‘teeth’ in many US, EU and Japan agreements likely leaves project developers in the DRC, Zambia and elsewhere still benchmarking offtake and financing terms against Chinese-backed deals as the practical reference point.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.