China-light industrial strategy: implications for critical minerals projects

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

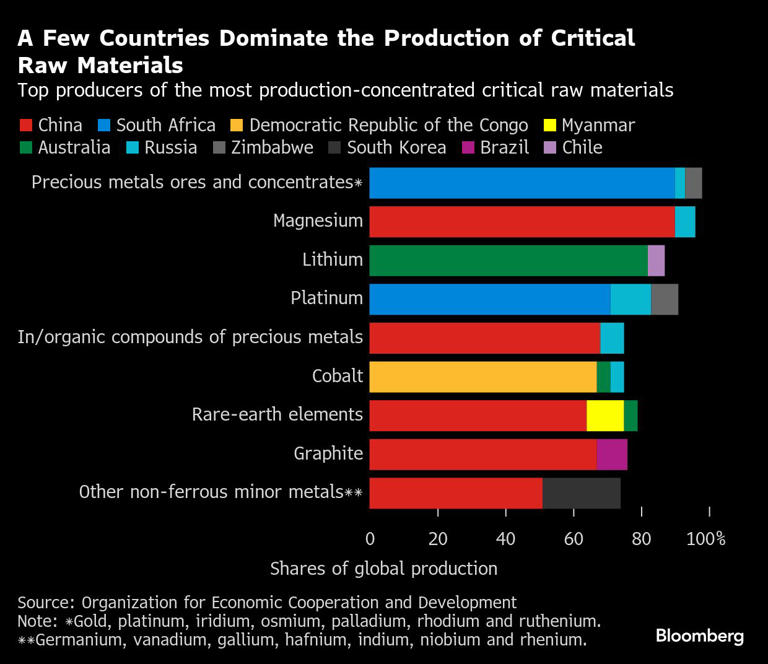

Western governments are adopting a “China-light” industrial strategy, pouring tens to hundreds of billions into defence, semiconductors and critical minerals via tools such as the US Defense Production Act, CHIPS and Science Act ($53 billion), and the EU’s €43 billion European Chips Act and Critical Raw Materials Act. China’s integrated model still dominates midstream capacity, refining 68% of global nickel, 73% of cobalt, 95% of manganese, all spherical graphite for battery anodes, and over 90% of rare earth processing and magnet production. For mining and materials players, the key shift is policy focus from new mines to midstream conversion capacity, long-term offtake-style defence contracts, and allied coordination of minerals and materials flows.

Technical Brief

- US use of Defense Production Act authorities now extends to strategic mining, processing and accelerated permitting.

- Inflation Reduction Act channels roughly $370 billion into energy and industrial transformation, reshaping metals and materials demand.

- EU’s European Defence Industrial Strategy pushes joint procurement and consolidation, affecting defence steel, alloys and component suppliers.

- Japan’s Economic Security Promotion Act explicitly targets “sensitive supply chains”, including critical minerals and advanced materials inputs.

- Pentagon-directed coal purchases under Trump show willingness to use defence offtake to prop specific energy commodities.

- Wars in Ukraine and Gaza exposed munitions production bottlenecks, linking explosives precursors and metals supply to strategic risk.

- Western interventions risk remaining episodic without permanent coordination bodies to manage minerals, processing and manufacturing capacity.

Our Take

In our Policy coverage on critical minerals, the Mountain Pass mine and MP Materials are among the few named non-Chinese rare earths assets, underscoring how concentrated Western supply options are compared with China’s 90%+ share of processing and magnet output.

The scale of U.S. and EU industrial commitments for semiconductors and clean energy (CHIPS and Science Acts plus the Inflation Reduction Act) is large in absolute terms, but when set against China’s dominance in refining of nickel, cobalt, manganese and spherical graphite, it signals that midstream processing capacity—rather than mine approvals alone—will be the main bottleneck this decade.

With China controlling the overwhelming majority of gallium, germanium and solar panel manufacturing, Western defence-linked buyers such as the Pentagon will likely have to prioritise long-term offtake and stockpiling strategies for these niche inputs, not just for headline battery metals like cobalt and rare earths.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

QCDB-io

Comprehensive quality control database for manufacturing, tunnelling, and civil construction with UCS testing, PSD analysis, and grout mix design management.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.