WoodMac lithium demand to 2050: supply, capex and risk takeaways for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

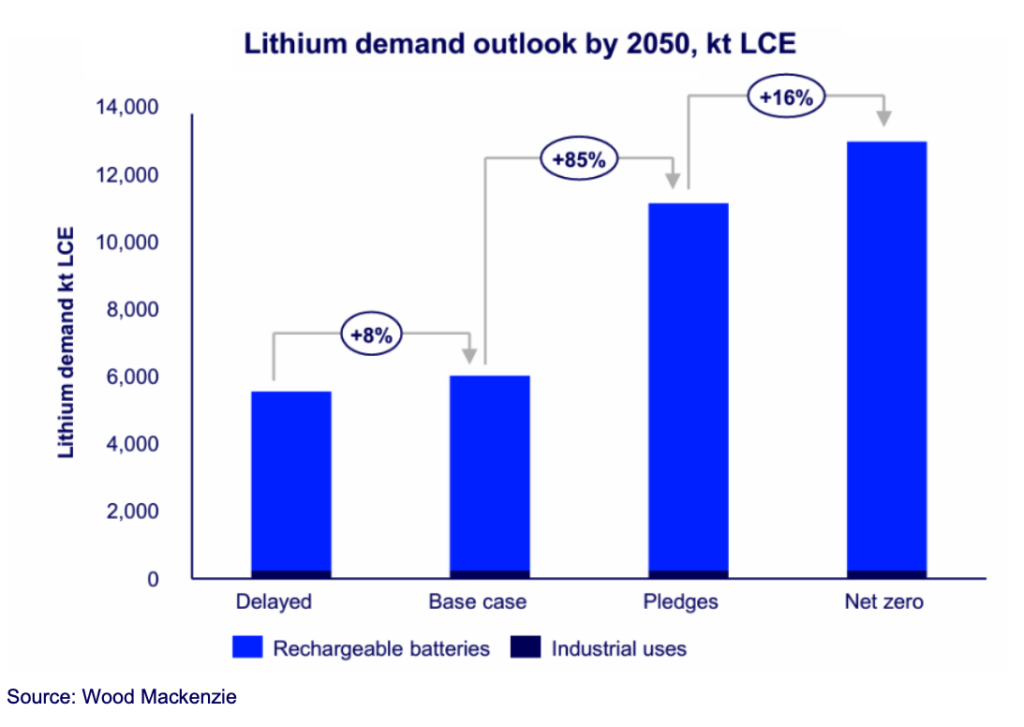

Global lithium demand is projected by Wood Mackenzie to reach up to 13.2 million tonnes LCE by 2050 under a net-zero pathway, with market deficits starting as early as 2028 and total sector investment needs ranging from $104 billion (delayed transition) to $276 billion (net zero). Electric vehicles account for 72%–80% of demand across scenarios, with EV penetration reaching 75% by 2040 under current country pledges and 95% under net zero, while grid-scale energy storage grows 6%–7% annually. Recycling is forecast to supply 2.3–2.7 million tonnes LCE by 2050, leaving 6.7–8.5 million tonnes of new supply still required, implying sustained pressure on new mines, refineries and regionalised supply chains from the 2030s.

Technical Brief

- Wood Mackenzie’s Energy Transition Outlook for Lithium defines four demand scenarios out to 2050.

- Scenario demand spans from 5.6 Mt LCE (delayed transition) to 13.2 Mt LCE (net zero) by 2050.

- Under delayed transition, supply remains adequate until about 2037 before deficits appear.

- Country pledges case requires an additional 6.7 Mt LCE of new supply by 2050.

- Net-zero pathway needs 8.5 Mt LCE extra supply by 2050, with deficits from 2028 onwards.

- Rechargeable batteries across all uses account for 96–98% of lithium consumption by mid‑century.

Our Take

With lithium and lithium carbonate appearing in over 100 keyword-matched pieces in our database, Wood Mackenzie’s 13–13.2 Mt LCE 2050 demand range effectively sets the high-end bookend that many recent project and pricing stories have lacked when framing long-term market size.

The projected 2.3–2.7 Mt LCE contribution from recycling by 2050 implies that even aggressive circularity leaves most supply coming from new mines, which will matter for operators in Australia, Latin America and the USA already facing permitting and social-licence constraints in our recent coverage.

The need for 6.7–8.5 Mt LCE of additional supply by 2050 suggests that diversified miners such as BHP, which feature frequently in our Mining category, are structurally better placed than single-commodity juniors to pivot capital from coal and gold into large-scale lithium projects as policy tightens towards net-zero pathways.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.