USA Rare Earth–Serra Verde deal: strategic and processing stakes for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

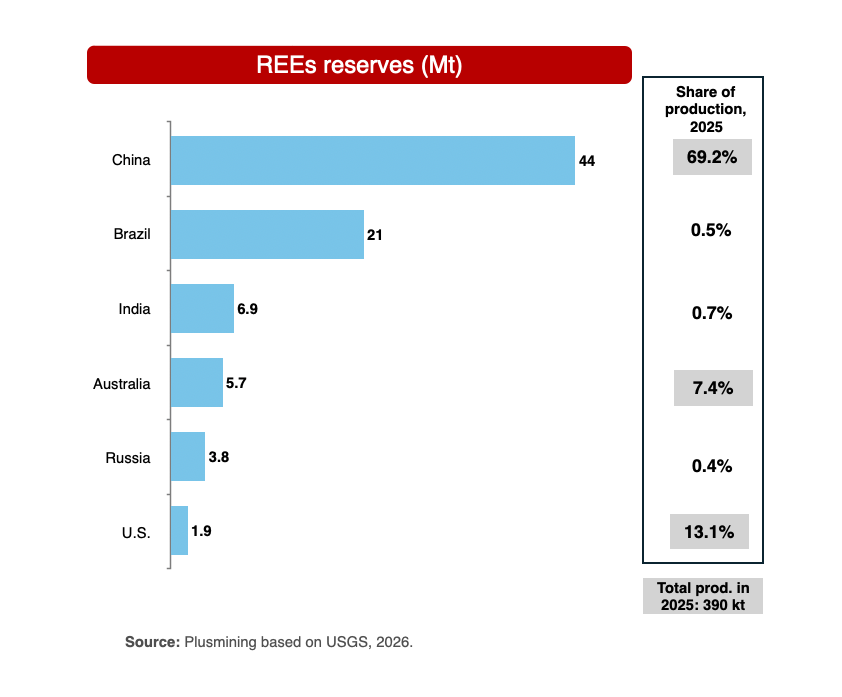

USA Rare Earth’s proposed US$2.8 billion acquisition of Serra Verde, owner of the Pela Ema ionic clay rare earth mine in Goiás, is emerging as a test case for whether Brazil can turn its rare earth geology into industrial power rather than another raw-material export cycle. With Pela Ema currently Brazil’s only producing rare earth operation, capable of supplying Nd, Pr, Dy and Tb for permanent magnets, the core issue is how CADE and Brasília link foreign capital to binding commitments on local processing, technology transfer and workforce development. The outcome will signal whether Brazilian rare earths feed a US-led mine-to-magnet chain on Brazil’s terms or primarily serve downstream value creation abroad.

Technical Brief

- Serra Verde’s Pela Ema in Goiás is one of the few ionic clay rare earth deposits outside China producing Nd, Pr, Dy and Tb.

- Strategic bottlenecks identified are midstream: separation, chemical processing, alloying and magnet manufacturing, not ore extraction.

- USA Rare Earth’s plan is to physically link Brazilian mine output to separation and magnet plants in the US and allied jurisdictions.

- CADE’s antitrust review is framed less around market share and more around Brazil’s leverage over downstream industrial development.

- Lula’s administration is building a National Policy on Critical and Strategic Minerals to shift from geology-led to industrial-policy-led project evaluation.

- Policy options discussed include conditioning foreign acquisitions on binding commitments for local processing, technology transfer, workforce training and environmental performance.

- Chile’s Aclara Resources Penco Module is cited as a parallel ionic clay rare earth project aiming at non‑Chinese mine‑to‑magnet integration in the Western Hemisphere.

Our Take

USA Rare Earth’s $2.8 billion Serra Verde deal in Brazil sits alongside its planned $1.2 billion NdFeB magnet plant in South Carolina and CHIPS Act-backed funding in the US, signalling a strategy to lock up both upstream rare earth supply in Goiás and downstream magnet capacity in North America.

China’s move to place USA Rare Earth on its export control list, as noted in our recent coverage, raises the stakes for Brazil: allowing a US-linked operator to consolidate Serra Verde could help diversify away from Chinese processing, but also entangles Brazilian rare earth policy in intensifying US–China technology competition.

Within our 141 keyword-matched rare earth pieces, Brazil has far fewer advanced projects than China or the US, so the outcome of CADE’s scrutiny of the Serra Verde transaction will likely shape how other Latin American jurisdictions, such as Chile with Aclara’s Penco Module, calibrate foreign control and value-add requirements for critical minerals.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

QCDB-io

Comprehensive quality control database for manufacturing, tunnelling, and civil construction with UCS testing, PSD analysis, and grout mix design management.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.