US copper tariffs outlook after critical minerals move: key points for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

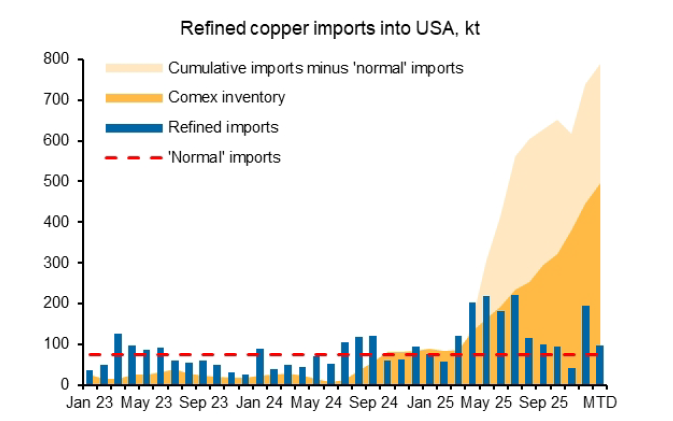

US copper tariffs now look less likely after the White House’s Section 232 decision on processed critical minerals directed the Commerce Department to pursue supply agreements first, with Macquarie’s Alice Fox saying this “significantly weakens the case for copper tariffs”. Comex copper inventories have already climbed about 412,000 tonnes since December 2024, with a further estimated 375,000 tonnes off-exchange, while CME-LME arbitrage for January–March has dropped to zero or negative, starting to pull metal out of US warehouses. A US-backed Mercuria–DRC joint venture giving US buyers first refusal on roughly 500,000 tonnes of copper and 40,000 tonnes of cobalt per year further supports a delay in any tariff decision, but a final rejection of tariffs could rapidly release US stocks and hit prices.

Technical Brief

- Section 232 outcome on processed critical minerals keeps tariffs as a contingent tool, not immediate policy.

- Silver’s 2024 experience shows tariff fears can spike Comex stocks, drain LBMA liquidity and lift lease rates.

- That silver dislocation reversed metal flows New York→London once exchange arbitrage flipped, a template now watched for copper.

- Negative CME–LME copper arbitrage has already drawn 8,700 t into LME sheds at New Orleans and Baltimore in one week.

- Elevated European copper premiums are diverting contract tonnage originally nominated for US delivery into EU markets.

- Macquarie notes US‑held copper is not yet priced for re‑export, but could be if ex‑China markets tighten.

Our Take

Macquarie also features in our late-2025 coverage of record LME copper prices driven by US stockpiling, so its view that US tariffs on refined copper are now less likely signals a potential softening of one of the demand-side drivers it previously highlighted.

With around 70% of US net refined copper imports at stake, any easing of tariff risk tends to favour established exporters in regions like Europe and Latin America, while putting more pressure on higher-cost US projects that were banking on protection to justify capex.

The sharp build in Comex silver inventories and the 10–30% order book declines flagged by Goldman in this copper-focused piece echo the volatility seen in our recent silver and copper price coverage, suggesting traders may lean more heavily on futures and inventory management rather than new mine supply through to the end of the year.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.