US copper glut and refining crunch: supply-chain takeaways for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

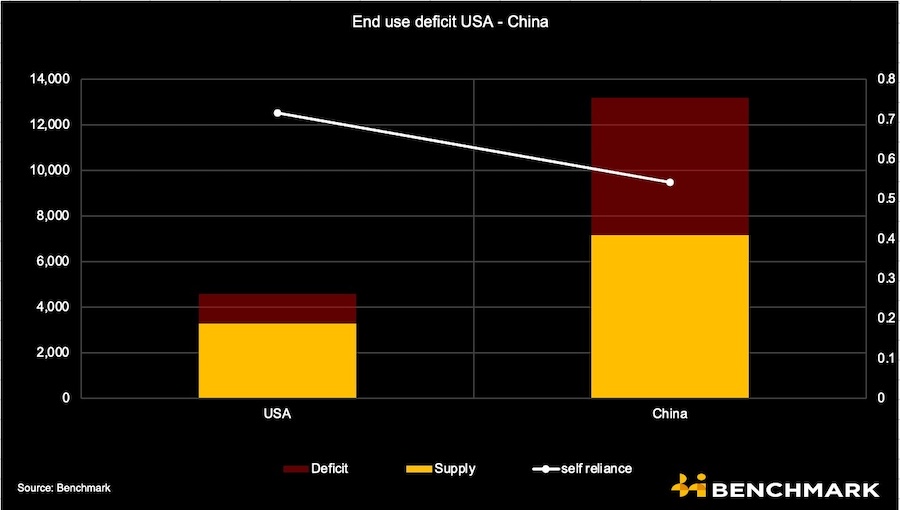

US copper supply can already cover 146% of domestic demand from mines and scrap, yet nearly 48% of US concentrate is exported because smelting and refining capacity is too small, leaving manufacturers reliant on imported cathode, Benchmark Mineral Intelligence reports. Analyst Albert Mackenzie argues that expanding US refining and scrap-processing capacity would do more for supply security than Washington’s Project Vault push for overseas mine ownership, as much US-controlled foreign output never returns home. Globally, Benchmark estimates 61 new copper mines and about $285 billion will be needed by 2030, with demand potentially reaching 50 million tonnes a year by 2050.

Technical Brief

- Resolution Copper in Arizona is reported to hold enough ore to cover ~25% of US copper demand.

- Benchmark notes US semi‑fabricators already consume substantial domestic scrap, implying latent capacity to shift further from primary ore.

- Mackenzie argues scaling US scrap-processing plants should precede further overseas mine acquisitions in any supply‑security strategy.

- Washington’s Project Vault focuses on US corporate ownership of foreign assets, including in the DRC, despite limited US refining pull‑through.

- Benchmark contrasts flows: a higher proportion of Chinese‑owned overseas mine output returns to China than US‑owned output returns to the US.

Our Take

The projected need for 61 new copper mines and $285 billion in capex by 2030 aligns with other copper pieces in our database that show majors like BHP and Rio Tinto increasingly prioritising very large, long-life assets, which tends to crowd capital away from mid-tier greenfield projects in higher-risk jurisdictions such as the DRC and parts of Latin America.

With US mine and scrap output already covering 146% of domestic copper demand but 48% of concentrate being exported, smelter and refinery investors in the United States face a different risk profile from greenfield miners: their bottleneck is permitting and power pricing rather than ore availability, especially compared with China where only 40% of demand is domestically supplied.

The sharp rise in copper’s energy-transition share of demand (from 7% to a projected 23%) echoes other copper-tagged coverage where OEMs and grid developers are starting to seek more direct offtake or JV positions in upstream projects, which could change the traditional miner–smelter–fabricator balance in markets like Arizona hosting assets such as Resolution Copper.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.