Tungsten and critical minerals: investment shift and CDOI lens for project teams

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

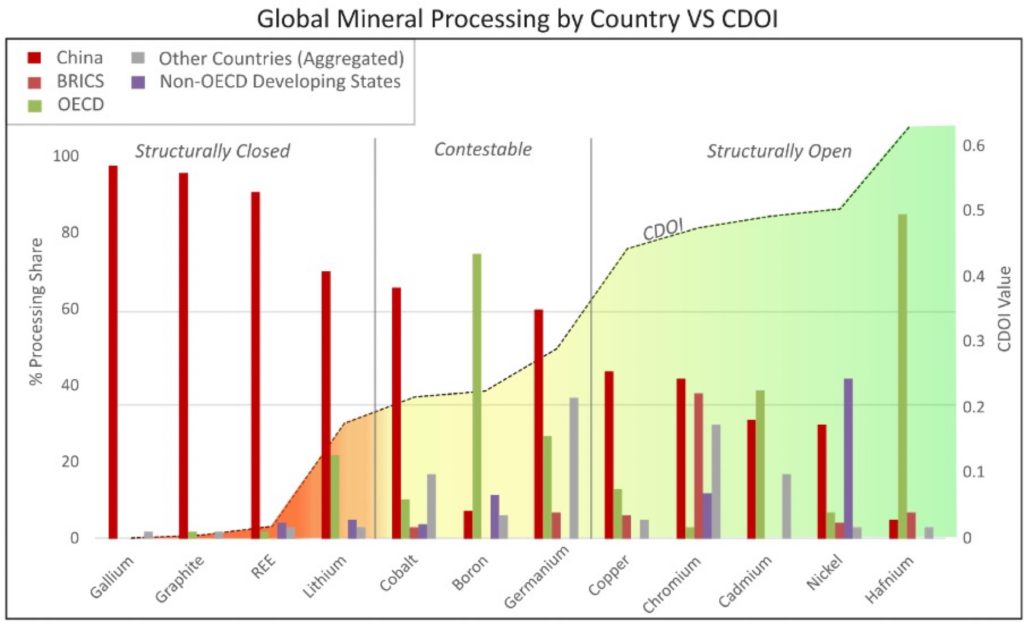

China’s structurally closed midstream processing dominance in gallium, graphite, rare earths, lithium and tungsten is described as effectively impossible to dislodge, prompting Nicholas Vafeas to propose a “Critical Dominance Opportunity Index” (CDOI) to measure where new entrants can still gain leverage. Base metals such as copper, nickel and chromium remain contestable, whereas tungsten shows how China is now moving to monopolise circularity frameworks and secondary processing of tungsten waste streams. The argument is that Western €10 billion-scale investments must shift from “catch-up” refining in closed markets to contestable midstream and recycling niches where strategic control is still achievable.

Technical Brief

- Structurally closed midstream markets are defined as those where new capacity cannot rationally displace incumbent ecosystem advantages.

- Ecosystem dominance is framed as thousands of incremental logistics, know‑how and supplier advantages, not just plant capacity share.

- Loss of coordination in these OECD‑dominated niches is identified as a specific backdoor for rapid hostile consolidation.

- Tungsten is used as a worked example where industrial waste and secondary streams become the next strategic battleground.

- China’s tungsten strategy is described as extending existing midstream control into recycling and circularity standards, not changing course.

- Policy distinction is drawn between capital for resilience (domestic redundancy, stockpiles) versus capital for future dominance (contestable midstream).

Our Take

Coverage tied to Australia, Canada and the USA in our Mining stories increasingly links critical raw materials to permitting and ESG constraints, which suggests that securing domestic supply of tungsten, gallium and hafnium will likely hinge as much on social licence and processing footprints as on ore discovery.

China appears frequently across our critical raw materials coverage as a dominant processor of graphite, rare earth elements and gallium, implying that any investment ‘paradigm shift’ discussed here will probably revolve around de-risking that midstream dependence rather than just opening new mines in Latin America or Europe.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.