Lithium pricing risk, not demand: project economics lens for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

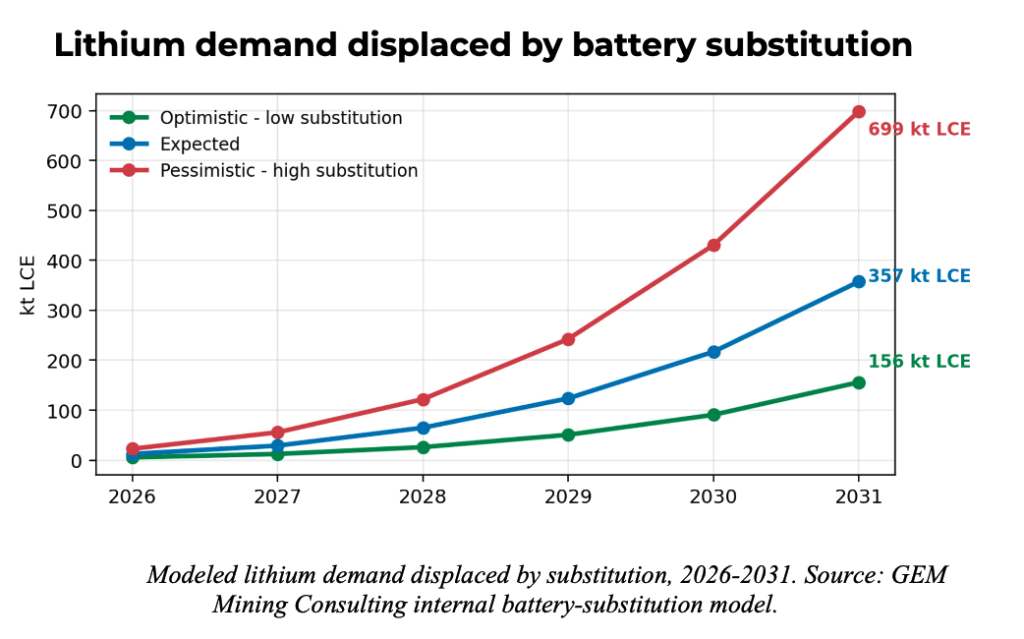

Battery substitution between 2026 and 2031 will cap lithium’s pricing power rather than displace it, with GEM Mining Consulting CEO Juan Ignacio Guzmán estimating sodium-ion and other chemistries could remove 357,000 tonnes LCE demand by 2031, about 12.5% of projected battery use. Sodium-ion, iron–air and flow batteries are gaining ground in stationary storage, low-cost mobility and industrial backup where energy density is secondary to cost, safety and cycle life. Chile’s brine rents, Argentina’s project pipeline valuations and Australia’s hard-rock margins all become more exposed to lower-for-longer lithium prices, pushing producers towards tighter cost control and process innovation.

Technical Brief

- Stationary storage buyers (utilities, grid operators) are prioritising capex/opex, safety and cycle life over volumetric energy density.

- Iron–air and flow batteries are specifically cited as contenders for grid-scale and industrial backup applications.

- Chile’s fiscal exposure is concentrated in a few large brine operations where state lithium rents are material.

- Argentina’s key vulnerability lies in valuation of a “vast” pre-production project pipeline reliant on bullish price decks.

- Australia’s hard-rock sector is flagged as most exposed to price swings via conversion margins and volume leverage.

- Future lithium projects needing very high incentive prices for bankability are expected to face tougher financing scrutiny.

Our Take

GEM Mining Consulting also appears in recent coverage of Venezuela’s mining reset and US rare earth processing strategy, signalling that its lithium pricing and substitution views are being shaped alongside broader critical-mineral policy work rather than in isolation.

The 12.5% potential displacement of battery demand by substitutes to 2031 aligns with other lithium-tagged pieces in our database that flag sodium-ion and flow batteries as commercially relevant mainly in China and Europe first, which could leave Latin American brine projects more exposed to price swings than to outright demand loss.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.