IEA copper supply warning: sulphuric acid pinch points explained for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

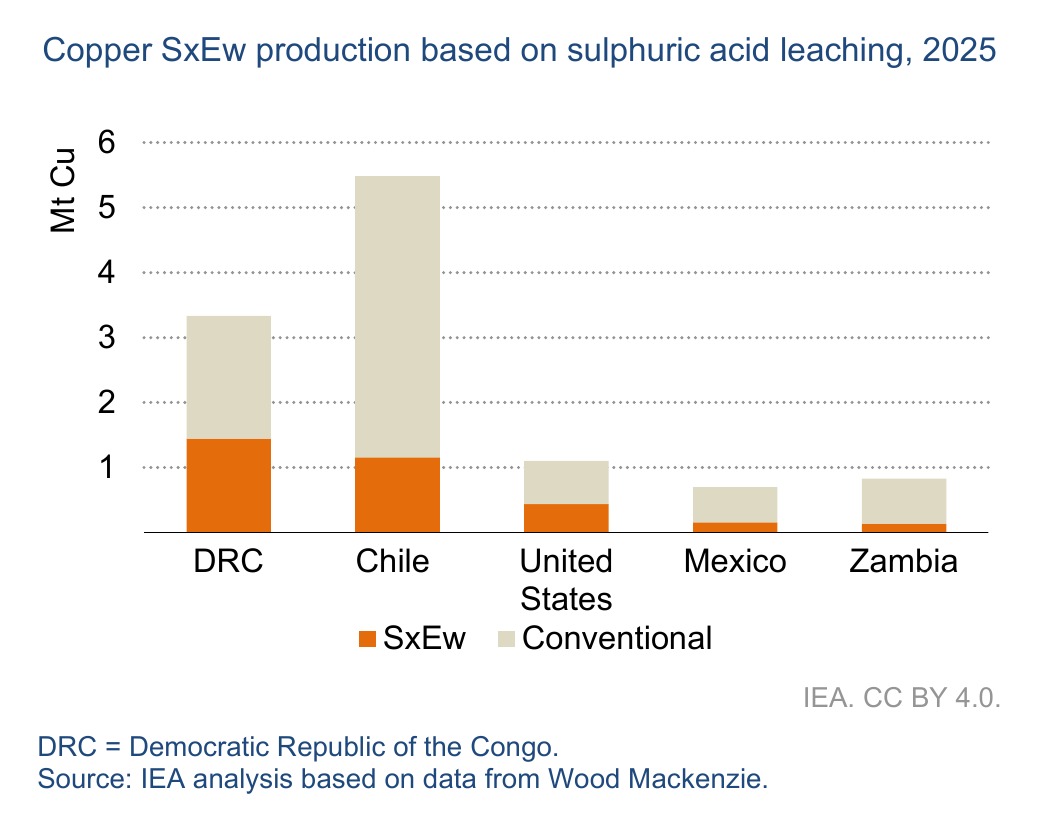

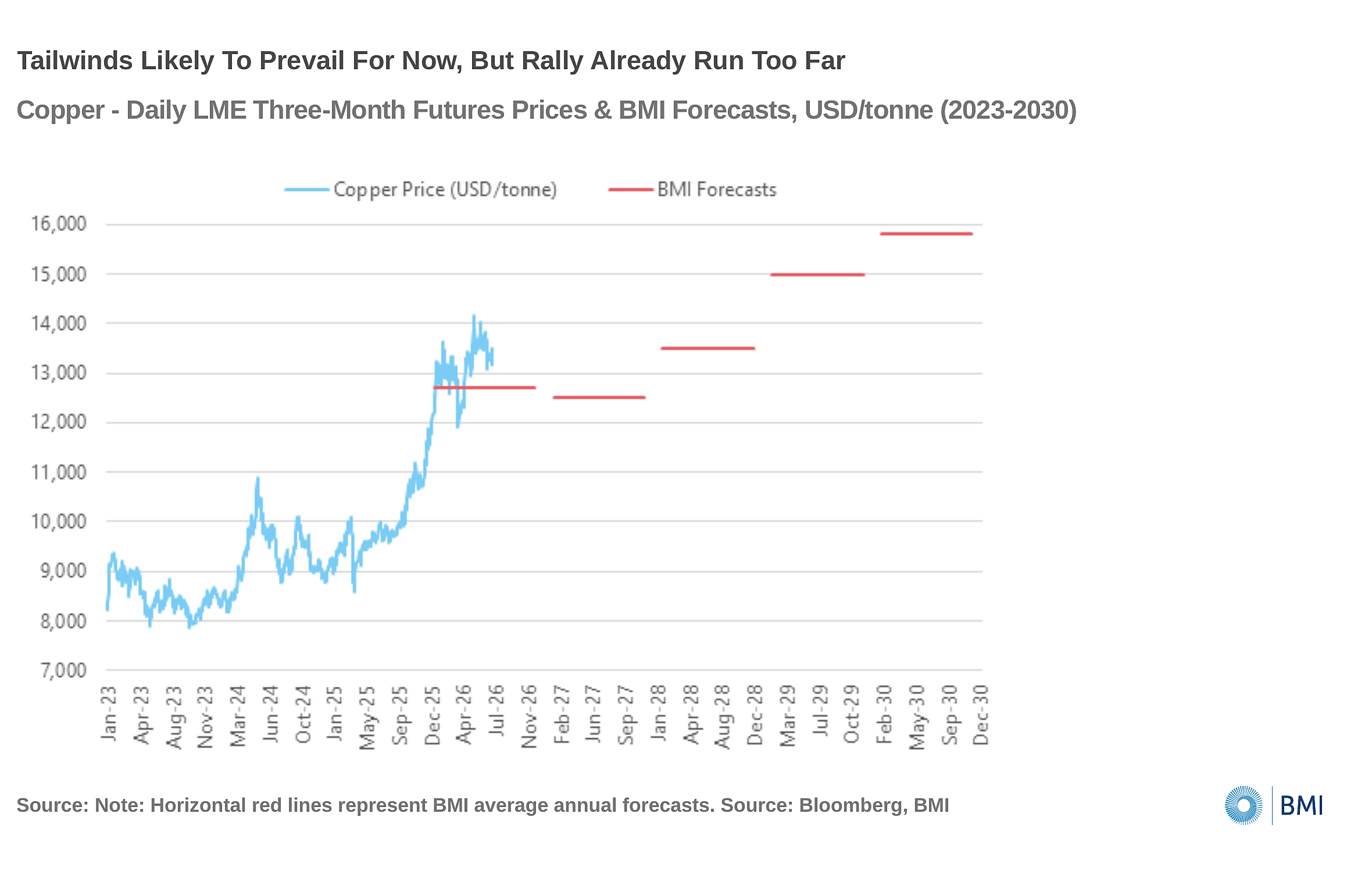

Copper supply risks have “worsened considerably”, with the IEA warning that sulphuric acid shortages now threaten more than 15% of global primary output produced via SxEW, after the effective closure of the Strait of Hormuz cut roughly half of global seaborne sulphur trade and China banned acid exports through year-end. The DRC and Chile are most exposed, with about 1.5 Mt and 1.2 Mt of leached production and some sites down to 30–60 days of sulphur/acid inventory, while 2025 disruptions already removed 1.5 Mt of mined supply and pushed prices above $14,000/t. Despite project additions in the DRC, Zambia, Peru, Russia and Canada, the IEA still sees primary supply around 25% short of 2035 requirements, with ore grades down 40% since 1991 and copper needing roughly $310 billion of the $750+ billion mining and refining investment required to 2040.

Technical Brief

- Sulphuric acid accounts for ~13% of SxEW operating costs on average, rising to ~20% in the DRC.

- Gulf countries and Iran supply ~25% of global sulphur, with ~50% of seaborne sulphur flows routed via Hormuz.

- China’s sulphuric acid export ban removes almost one-quarter of ex‑China acid availability through year-end.

- Grasberg’s 2025 mudflow cut production to ~50% of 2024 levels, with full recovery only expected by 2028.

- Flooding at Kamoa‑Kakula reduced 2025 output by nearly one‑third versus guidance and drags 2026 below 2024 tonnage.

- Benchmark treatment charges for 2026 settled at $0/t, with spot TC/RCs negative since 2024 despite record prices.

- Chinese smelters now provide ~50% of global refined output, with utilisation ~85% versus <70% outside China.

- Planned Chinese smelter additions of ~2 Mt have been halted, and existing capacity cuts exceed 10% for 2026.

- Capital intensity for brownfield copper expansions has risen ~65% since 2020, approaching typical greenfield unit costs.

Our Take

The projected 25% copper supply shortfall by 2035, alongside 17‑year discovery‑to‑production lead times, suggests that late‑stage projects like Resolution, Baimskaya and Lumwana expansions will likely command a premium in M&A processes, consistent with the 20% jump in global mining deal value flagged in the IEA data.

With over 15% of global primary copper output coming from SxEW and acid making up to 20% of costs in the DRC, the current sulphuric acid squeeze effectively shifts cost curves against leach‑heavy districts such as the DRC and Chile, putting conventional sulphide operations at assets like Antamina and Highland Valley in a relatively stronger strategic position.

Our database shows multiple recent copper‑price pieces citing Macquarie and Goldman Sachs turning more bullish as prices approach $6.3/lb, and the IEA’s call for roughly $310 billion of copper investment to 2040 provides the long‑term demand narrative underpinning those higher price decks despite Macquarie’s near‑term view that prices are ahead of fundamentals.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.