De Beers’ Gen Z diamond rebound: demand signals and price outlook for miners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

Gen Z buyers are driving a rebound in US natural diamond demand, accounting for 23% of value while only 18% of the population, with average spend per purchase of $4,080 versus $2,250 for Baby Boomers and average stone sizes rising to 1.86 carats. De Beers’ data from 950 independent US jewellers show natural diamonds still command 85% of diamond jewellery sales value, despite lab-grown competition and total natural supply falling towards 90 million carats, the lowest since 1987. For Botswana, Angola, Namibia, South Africa and Lesotho, stabilising US demand and the Luanda Accord’s 1% rough-revenue marketing fund could support mine revenues and rough prices after several weak years.

Technical Brief

- De Beers’ US Diamond Acquisition Study surveyed 18,500 women, giving unusually granular demand segmentation data.

- Natural diamonds were the top-ranked luxury gift for 11% of respondents, ahead of lab-grown at 8%.

- Coloured gemstones and plain gold trailed far behind in stated desirability, at 5% and 4% respectively.

- Average natural diamond jewellery ticket prices rose 25% year-on-year, from $3,242 to $4,063.

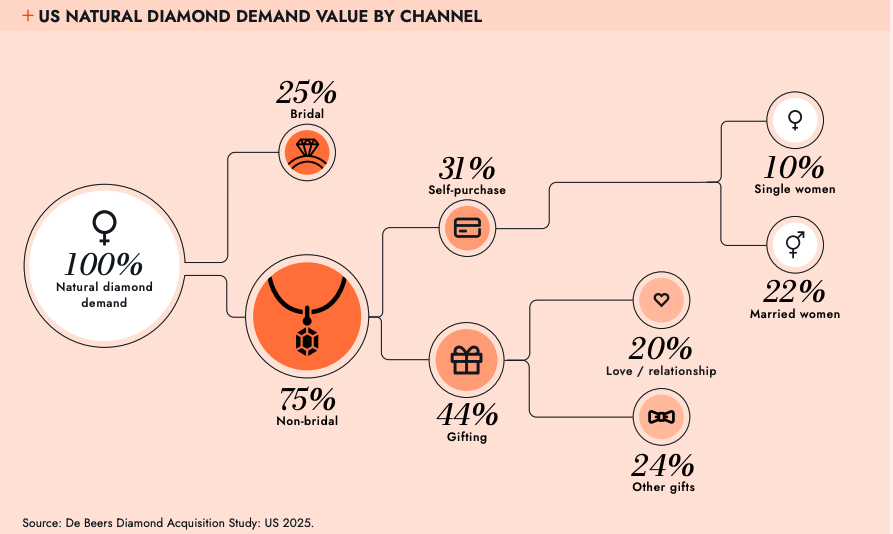

- Bridal still dominates but only accounts for 45% of Gen Z natural diamond demand, indicating diversification of use-cases.

- Non-bridal purchases now include promotions, career milestones, birthdays and self-reward, smoothing demand beyond engagement seasonality.

- De Beers–Signet “Worth the Wait” campaign (launched October 2024) targets Zillennials with milestone-focused messaging.

- Luanda Accord allocates 1% of rough diamond revenues to a Natural Diamond Council marketing fund.

- Analyst Paul Zimnisky estimates 2026 natural diamond supply at ~90 million carats, the lowest since 1987.

- Zimnisky reports early rough-price support, suggesting tightening supply–demand balance after four years of contraction.

Our Take

The rebound in natural diamond demand that De Beers is attributing to Gen Z comes as Anglo American has written De Beers down to $2.3 billion and is exploring an exit, so sustained US bridal and gifting demand will be central to any valuation case for potential buyers such as Botswana’s proposed sovereign-backed vehicle.

With natural diamond supply estimated around 90 million carats versus 150 million carats historically, De Beers’ upstream technology push noted in our recent coverage suggests a parallel strategy: squeeze more value from a structurally tighter supply base through higher average prices and improved recovery rather than chasing volume growth.

In our database of diamond-tagged mining pieces, only a handful link consumer behaviour metrics (like Gen Z’s 23% share of US natural diamond demand) directly to upstream strategy, which signals De Beers is unusually explicit in tying mine-side decisions and marketing spend (e.g. the 1% Luanda Accord contribution) to retail demographic data.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.