Copper rally and 2026 earnings: project and capex implications for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

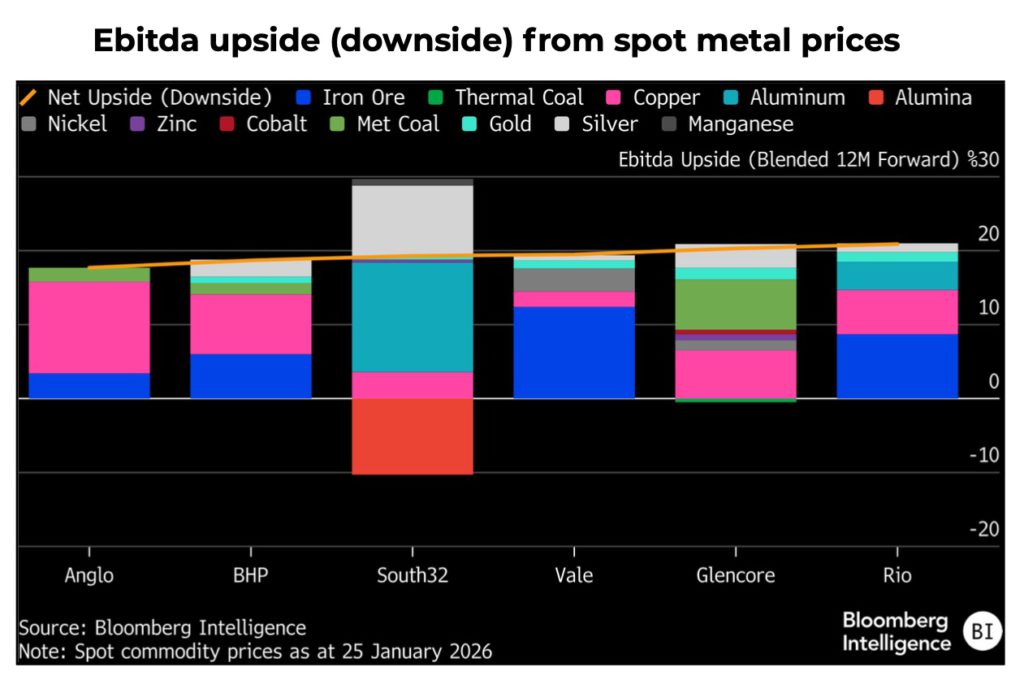

Copper’s price rally is setting up one of the strongest earnings years since early 2025 for diversified miners, with spot levels implying 18%–21% upside to 2026 consensus Ebitda and Rio Tinto and Glencore each showing about 20%–21% potential. Copper is projected to generate over 35% of diversified miners’ 2026 Ebitda, with Anglo American’s Teck deal pushing its copper share above 70%, BHP nearing 50%, Glencore about 35% and Rio at roughly 26% versus 47% from iron ore. Execution risk looms as Glencore advances Coroccohuayco and the Alumbrera restart, BHP progresses Jansen and the Vicuna study, and Vale pursues a plan to double copper output by 2030.

Technical Brief

- Spot prices imply 18%–21% upside to one‑year forward consensus Ebitda for major diversified miners.

- Rio Tinto’s 2026 Ebitda forecasts have already risen 18% in six months, yet spot still implies +21%.

- Glencore’s 2026 Ebitda has only increased 5% over the same period, leaving more headroom for upgrades.

- About two‑thirds of Glencore’s spot‑implied Ebitda upside comes from metallurgical coal and copper price strength.

- Precious metals are non‑core for Glencore yet gold and silver add over 4% to its implied upside.

- Copper’s Ebitda share for diversified miners is up ~14 percentage points versus eight years ago, driven mainly by prices and portfolio pruning.

- Rio Tinto has lifted copper output 54% since 2019 via Oyu Tolgoi ramp‑up, versus BHP’s 11% increase.

- Stronger earnings revisions may encourage scrip‑funded M&A, but raise execution risk on unde‑risked copper growth pipelines.

Our Take

The projected 24–28% 2026 Ebitda growth for copper‑heavy Glencore and Anglo American aligns with our recent coverage of Rio Tinto–Glencore merger talks, where analysts argued that consolidating large copper portfolios would be one of the main value drivers rather than coal or iron ore exposure.

Anglo American’s pro‑forma copper earnings share above 70% and BHP’s near‑50% tilt mean both are structurally more leveraged to the 16–25% copper price uplift scenarios than Rio Tinto, which our database still shows as primarily iron ore‑weighted despite the Oyu Tolgoi ramp‑up.

Vale’s plan to double copper output by 2030 positions it as a late but aggressive entrant into the copper‑weighted diversified peer set tracked across our 784 Mining stories, potentially narrowing the strategic gap with BHP and Anglo on energy‑transition metals exposure.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.