Zimbabwe export ban: Fitch’s BMI lithium outlook and pricing notes for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

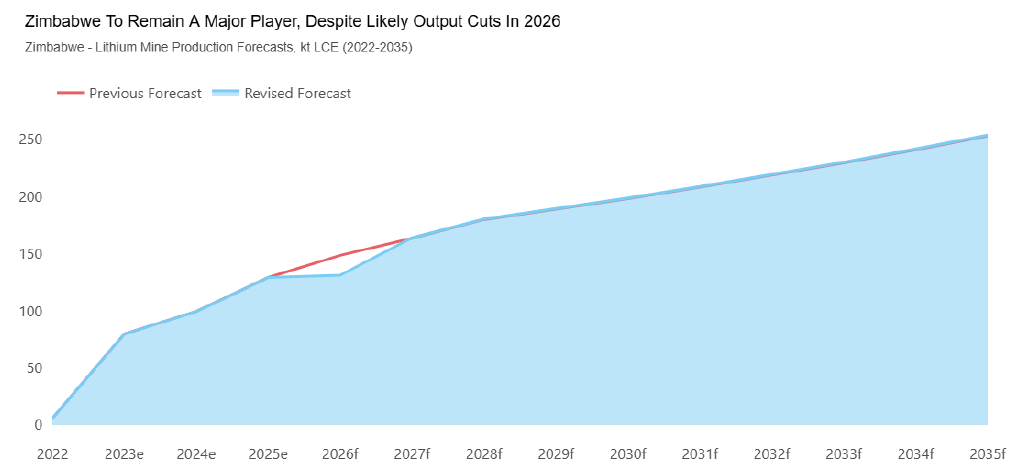

Zimbabwe’s immediate ban on exports of raw minerals, including lithium concentrates, is expected by Fitch’s BMI to tighten the lithium market only temporarily, with Zimbabwe currently supplying about 10% of global output and mine production now forecast at 131,100 tonnes LCE in 2026. Huayou Cobalt’s Arcadia plant, due online shortly, will process only its own concentrates, leaving other operators such as Sinomine Resources’ Bikita mine and the state-owned Kamativi mine to curb production until their planned lithium sulphate plants ramp up from mid-to-late 2027. BMI has lifted its 2026 Chinese lithium carbonate and hydroxide price forecasts to $13,500/tonne and $13,000/tonne respectively, warning that prolonged disruptions could sustain higher prices.

Technical Brief

- Export of lithium concentrates was banned immediately in late February, nearly three years earlier than planned.

- Earlier 2022 restrictions had already prohibited export of unprocessed lithium ore, pushing miners towards concentrate production.

- Huayou Cobalt’s Arcadia processing plant will be dedicated to in‑house feed, excluding third‑party concentrates.

- Additional lithium sulphate plants are planned at Sinomine’s Bikita mine and the state‑owned Kamativi operation from 2027.

- Democratic Republic of Congo’s 2025 cobalt export curbs were later converted into a quota system after market disruption.

- DRC controls about 75% of global cobalt output, so its export constraints directly escalated battery‑grade cobalt costs.

- Zimbabwe’s policy is expected by BMI to be more effective at attracting local processing investment than DRC’s approach.

Our Take

With Zimbabwe accounting for about 10% of global lithium output in our database, any export disruption mainly affects spodumene and concentrate flows to Chinese converters such as Huayou Cobalt and Sinomine rather than total battery‑grade chemical availability, which is still dominated by Australia and South America.

BMI’s recent industrial metals outlook (Feb 2026) also flagged lithium alongside nickel and tin as particularly sensitive to policy and supply shocks, so a Zimbabwe ban reinforces their thesis that price volatility will be driven more by episodic regional interventions than by long‑term resource scarcity.

The combination of Zimbabwe’s lithium position and the DRC’s roughly 75% share of world cobalt production concentrates two key battery inputs in central and southern Africa, which in our coverage has been pushing OEMs and traders to diversify into Brazil and other jurisdictions despite higher operating and permitting hurdles there.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.