Middle East conflict and metals markets: supply risk lens for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

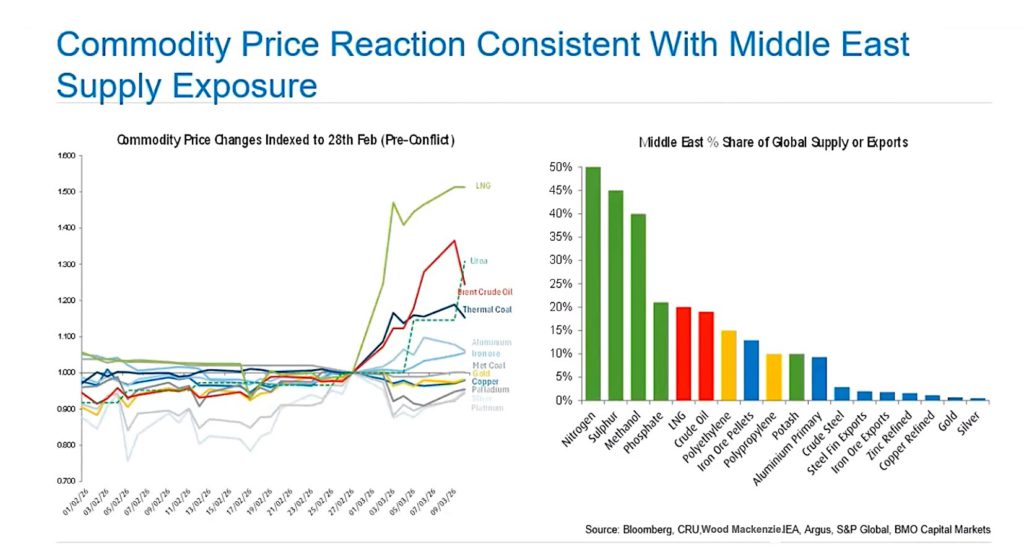

US–Israel military action against Iran has driven oil briefly towards $120 per barrel before settling in the $90s, as tanker traffic through the Strait of Hormuz has fallen from about 80 ships per day to only a handful, erasing expectations of near‑term oversupply. BMO analysts report nitrogen fertiliser prices up roughly 30%, with Middle Eastern producers supplying nearly half of global urea exports and about 15% of global polyethylene capacity, pushing utilisation towards 90%+. Metals impacts are uneven: up to 5 Mt of Middle Eastern aluminium output may be disrupted, while sulfur‑intensive nickel and phosphate chains face rising cost and supply risk.

Technical Brief

- International Energy Agency members have agreed their largest-ever coordinated release of strategic oil reserves.

- Storage bottlenecks and refinery outages are compounding seaborne constraints, tightening downstream petroleum product availability.

- Polyethylene supply from the Middle East, at ~15% of global output, is shifting global utilisation from oversupplied to tight.

- Successive polyethylene price increases have already been announced in the US and Europe as contracts reset.

- Higher sulphur and feedstock prices are expected to lift margins for titanium dioxide producers such as Tronox and Chemours.

Our Take

The potential disruption of up to 5 Mt of Middle East aluminium supply in this piece lines up with later coverage of Aluminium Bahrain’s force majeure and the effective closure of the Strait of Hormuz, which our database links to aluminium prices moving above $3,300–3,400/t on the LME.

With nitrogen prices already up around 30% in this conflict snapshot, subsequent items on Nutrien and other fertiliser producers suggest that North American and Australian nitrogen and potash assets are likely to enjoy a temporary margin tailwind, but also face higher volatility in input costs and logistics.

The article’s focus on oil, gas and petrochemical flows through the Middle East complements a cluster of recent ‘Projects’ stories in our mining coverage where copper, nickel and battery metals developers in Africa and Latin America are stress‑testing project economics against sustained $90+/bbl oil scenarios for fuel and reagent costs.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.