India rises as China slows: demand shift implications for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

Vale’s push to expand iron ore shipments into India, alongside BHP’s first cargo to the country after China’s ban, signals a structural shift as India’s steel demand climbs from 32 million tonnes in 2004 to 148 million tonnes in 2024 while China’s eases from a 1‑billion‑tonne peak to about 857 million tonnes. India’s electricity demand is forecast by the IEA to grow 6.4% annually to 2030, adding over 570 TWh in five years and driving higher requirements for copper, aluminium and battery metals. For miners, China remains the price anchor, but marginal growth in ferrous and electrification metals is increasingly tied to India’s infrastructure-heavy build‑out.

Technical Brief

- Vale’s CEO projects India’s steel output could double by the end of the decade, guiding long-term iron ore blending and logistics planning.

- BHP’s February commentary links Chinese iron ore demand softness directly to structural weakness in real estate construction.

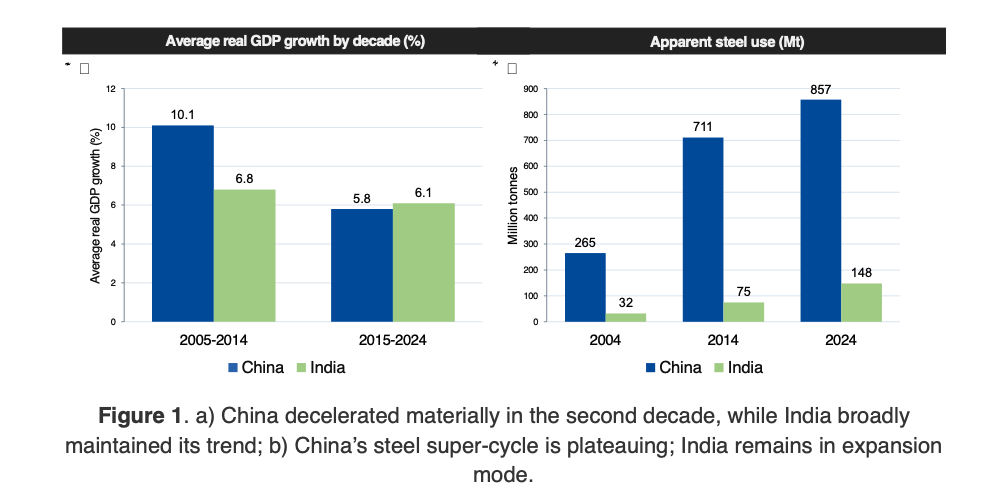

- China’s real GDP growth decelerated from ~10.1% (2005–2014) to ~5.8% (2015–2024), reducing construction-led metal intensity.

- India’s GDP growth held at ~6.8% then ~6.1% across the same periods, sustaining infrastructure-led commodity demand.

- GDP per capita divergence (China ~$13,300 vs India ~$2,700 in 2024) indicates India is earlier in the metal‑intensive build-out phase.

- China’s apparent steel use peaked above 1 billion tonnes in 2020 before easing to ~857 Mt in 2024.

- India’s apparent steel use rose steadily from 32 Mt (2004) to 148 Mt (2024), without evidence yet of saturation.

- Intensity-of-use framing implies China’s demand shifts towards grids, EVs, batteries and machinery, while India’s remains construction-heavy.

- For mine planning and marketing, China is expected to stay the largest absolute consumer, but marginal tonnage growth is now modelled primarily on India and other emerging Asian economies.

Our Take

Vale’s prominence in our recent coverage on iron ore and copper – including reserve growth plans to 2027 – suggests majors are already repositioning portfolios for a world where China’s 1 billion‑tonne steel plateau coexists with structurally higher Indian steel and power demand.

With India’s electricity demand projected to grow 6.4% annually through 2030, the implied pull on coal, copper and aluminium gives Western Canada (British Columbia, Alberta, Saskatchewan, Yukon, Northwest Territories) a potential demand outlet that aligns with several Canada‑focused base‑metals and coal project stories in our database.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.