Gold, silver, copper price plunge: risk and project signals for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

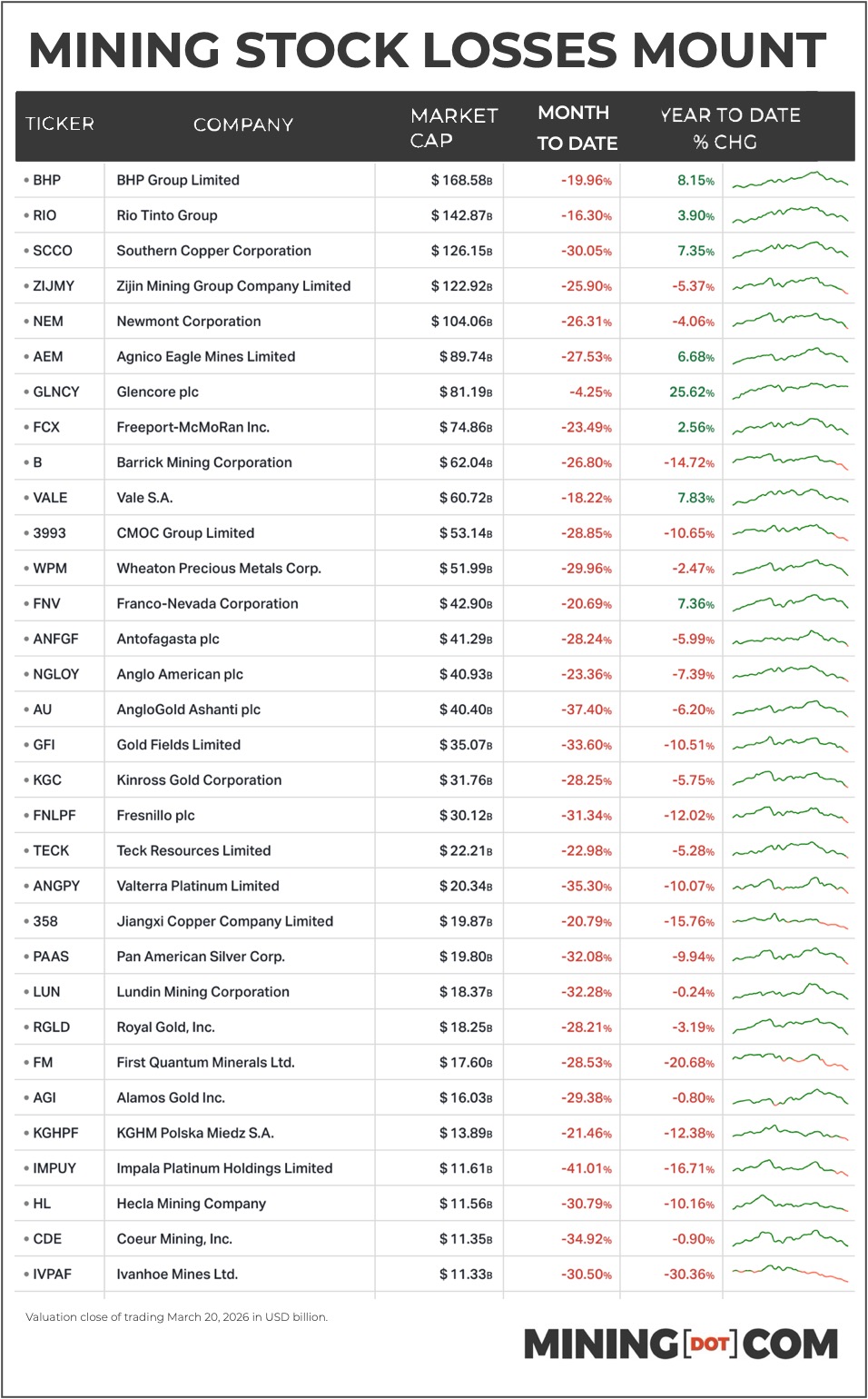

Billions were wiped off mining equities as gold, silver and copper all entered technical bear markets, with gold futures dropping $225/oz on Friday to $4,492/oz (down over 20% from the 29 January peak), silver sliding 44% from its high and copper losing nearly $2,800/t from its record. Newmont, Barrick and AngloGold Ashanti are down 26–37% since the Iran war began, while copper-focused majors such as Freeport-McMoRan, Southern Copper and First Quantum have fallen 23–31%, despite growth projects like Freeport’s proposed $7.5 billion El Abra expansion to add 300,000 t/y of copper. Glencore is the notable outlier, off only 4.3% since hostilities started and up 25.6% year-to-date, supported by trading around 4 million boe/d and exposure to surging coal and oil prices.

Technical Brief

- Newmont’s New York market cap has fallen from $143 billion in January to $104 billion.

- Barrick’s valuation is down $27 billion over the same period, now sitting at $62 billion.

- Anglogold Ashanti, Gold Fields and Kinross now sit at roughly $40b, $35b and $32b market caps respectively.

- Silver-focused Fresnillo and Pan American Silver have dropped to about $30 billion and under $20 billion valuations.

- BHP has lost 20% from a record $213 billion valuation, despite reporting record profits and strong Chinese demand.

- Rio Tinto’s 16.3% share decline to $143 billion comes as it commits $500 million to Resolution’s drilling.

- Freeport’s market value has retreated from briefly $100 billion in February to $74 billion after heavy trading.

- Zijin Mining’s US units are down 30.2%, yet it remains the fourth most valuable miner at $123 billion.

Our Take

The same set of gold and copper majors hit in this sell-off—Newmont, Barrick, AngloGold Ashanti, Freeport-McMoRan and others—were highlighted in our 26 February producer rankings piece as beneficiaries of a 2025 gold price surge, underscoring how quickly equity valuations are whipsawing around macro and conflict headlines rather than mine-level fundamentals.

With copper still around $5.3/lb despite a 7.4% weekly decline, large capex items like Freeport’s planned $7.5 billion El Abra expansion and Rio Tinto’s $500 million Resolution drilling campaign remain in a price environment that historically has supported long-life project sanctioning, but boards may now face pressure to re-test downside cases and timing.

The earlier 4 March coverage of the Iran–US conflict already showed these same diversified houses (BHP, Glencore, Rio Tinto, Vale, Anglo American, Teck) trading more on macro risk than on individual project news, which likely means near-term project pipelines in Australia, Canada and Chile will be managed with tighter capital discipline and higher return thresholds until volatility eases.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.