Gold price holds $4,000: funding and project pipeline risks for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

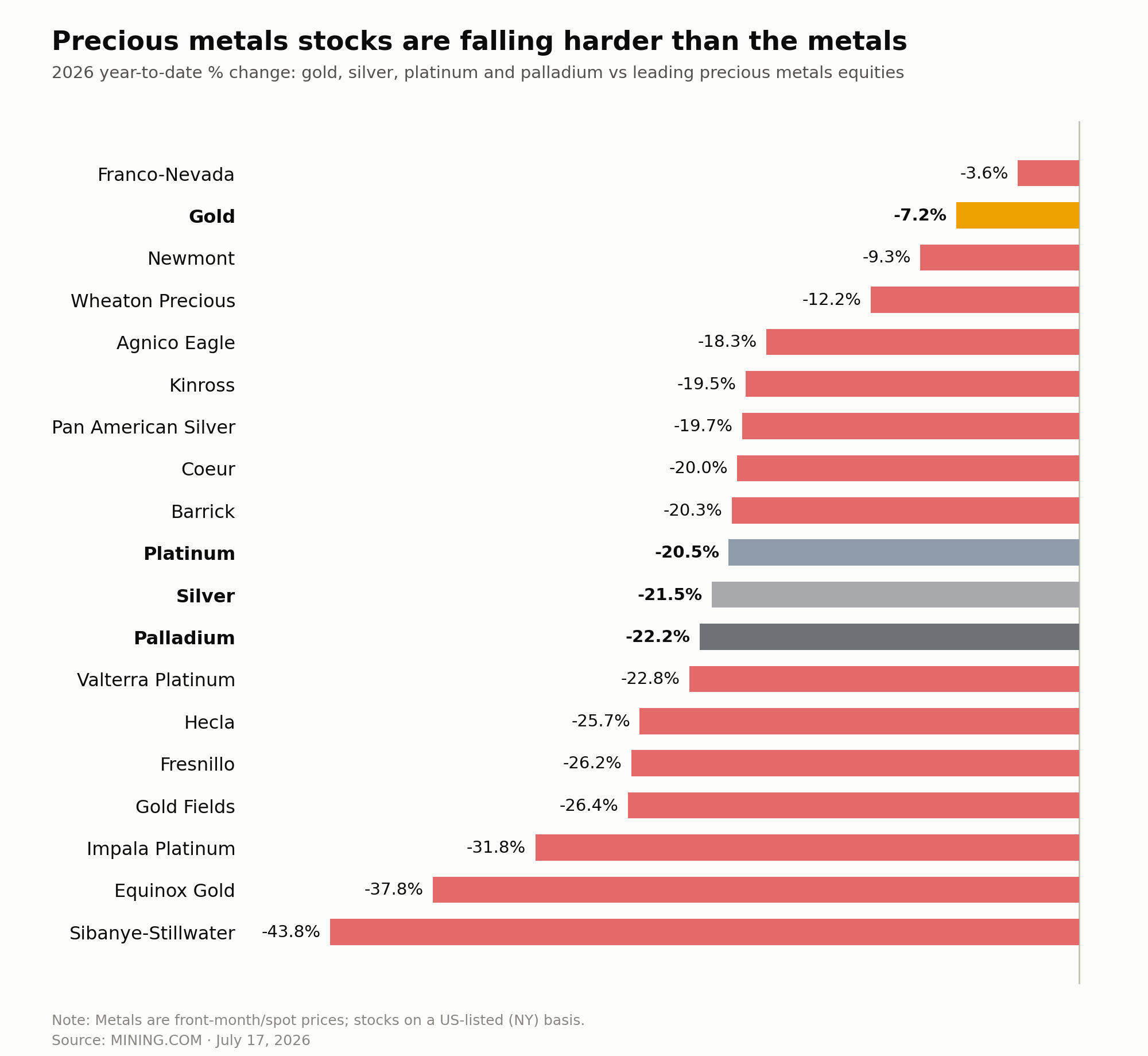

Gold is holding near $4,000/oz, with spot at $3,992 in New York and Comex futures back above $4,000, even after a 3% weekly drop and a 29% retreat from January’s ~$5,600 peak amid war-driven oil gains of almost 13% in five sessions and renewed Fed hike bets. Physical demand is weak, with Indian dealers quoting discounts up to $45/oz and Chinese premiums shrinking to par, while gold ETFs shed $8.9 billion in June. Equities are absorbing the real pain: the median leading US-traded gold and copper miner is ~38% below its 52‑week high, with Hecla 58%, Sibanye 62% and Equinox 54% off their peaks, signalling sustained funding and balance-sheet pressure for project pipelines.

Technical Brief

- June marked gold’s worst monthly performance since the 2008 financial crisis, per Morgan Stanley.

- Silver is down 21.5% year-to-date, with spot at $55.74/oz and an eight‑month low hit Friday.

- Platinum and palladium prices have fallen 20.5% and 22.2% respectively in 2026, deepening PGM revenue stress.

- Gold ETFs saw $8.9 billion outflows in June, including $5.5 billion from North American funds alone.

- Among majors, Franco-Nevada is down 3.6% YTD, versus Newmont -9.3% and Wheaton -12.2%.

- Equinox is almost 38% lower YTD, with Hecla -25.7%, Barrick -20.3%, Kinross -19.5% and Agnico -18.3%.

- PGM-focused Sibanye-Stillwater has lost 43.8% YTD, Impala Platinum 31.8% and Valterra Platinum 22.8%.

- From 52‑week highs, Sibanye is down 62%, Hecla 58%, Equinox 54%, Coeur 49%, Gold Fields 48%, Agnico 45%.

- The world’s 50 biggest mining companies collectively shed $228 billion in market value in Q2 as bullion fell 14%.

Our Take

The sharp 29% retreat in gold from its January peak lines up with Morgan Stanley’s April 2026 downgrade of its H2 2026 gold target to $5,200/oz, signalling that equity underperformance at names like Newmont and Barrick is occurring even against still historically elevated bullion levels in our database.

Caledonia Mining’s exposure to the Bilboes oxide open-pit mine in Zimbabwe means its project economics are now being tested under one of only five >25% gold drawdowns since 1960, which typically forces higher-cost African operations to revisit cut-off grades and mine plans rather than rely on price recovery alone.

With Sibanye-Stillwater, Impala Platinum and Valterra Platinum all showing deep year-to-date and from-peak losses while palladium and platinum are down over 20% in 2026, South African PGM producers in our coverage appear far more price-sensitive than diversified gold majors, increasing the likelihood of further shaft rationalisations and capex deferrals if prices stay at current levels.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.