Copper rally and smelting power shift: commercial risk notes for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

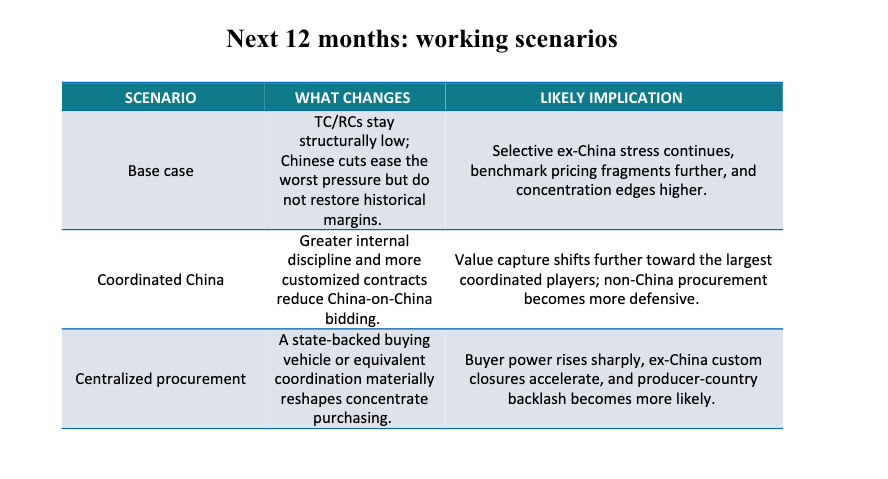

Copper’s near-record prices contrast with a collapse in treatment and refining charges, with annual TC/RC benchmarks plunging from about $80/t and 8.0 c/lb in 2024 to effectively zero by 2026 and spot terms turning negative through 2025, squeezing custom smelter margins. Governments and buyers are responding with coordination and support measures, from Australia’s A$600 million package for Mount Isa and Townsville to China’s push for disciplined capacity growth and centralised concentrate procurement via state-backed entities. For miners, the emerging risk is increased dependence on a smaller, more coordinated group of smelters, tighter blending rules and more customised, non-benchmark contracts that shift bargaining power downstream.

Technical Brief

- Smelter economics hinge on TC/RCs, by-product credits (sulphuric acid, gold, silver) and regional premiums.

- Chinese smelters have partially offset fee compression via stronger by-product credits, delaying but not removing margin stress.

- China already controls roughly 50% of global copper smelting capacity, amplifying any move to coordinated buying.

- Japan is consolidating concentrate procurement through Pan Pacific Copper, centralising negotiation and offtake risk for suppliers.

- European commentators describe a “silent crisis” in smelting, signalling uncompetitive costs and potential capacity attrition.

- Australia’s A$600 million package targets Mount Isa and Townsville smelting/processing hubs as strategic industrial infrastructure.

- Anticipated outcomes of prolonged low fees include smelter closures, direct subsidies and tighter inter-governmental/industry coordination.

- Longer-term, miners face greater reliance on smelters for both offtake and project finance as processing options consolidate.

Our Take

Our database shows copper and sulphuric acid appearing together across many of the 247 keyword‑matched pieces, which suggests integrated value strategies around acid (for leaching and fertiliser markets) will be increasingly important for smelters and refineries exposed to negative spot terms through 2025.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.