Lynas–Japan rare earths offtake: pricing floor and supply security for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

A revised offtake between Lynas Rare Earths and Japan’s JARE locks in annual purchases of 5,000 tonnes of neodymium‑praseodymium at a $110/kg floor price until 2038 and commits JARE to 50% of Lynas’ heavy rare earth output, including dysprosium and terbium. The deal decouples pricing from Chinese benchmarks used in the original 2011 $250 million agreement, offering Japanese magnet and electronics manufacturers a non‑Chinese supply chain anchored on Mount Weld ore and Malaysian separation capacity. Lynas, which produced 10,908 tonnes of rare earth oxides in 2024, saw its shares jump 16% to A$20.59.

Technical Brief

- Beijing’s export controls target dual-use technologies containing rare earths, directly affecting Japanese defence and electronics supply chains.

Our Take

The extension of the JARE offtake to 2038, noted in our 10 March 2026 coverage, effectively underpins long‑run demand for Mt Weld feed into Lynas’ Malaysian cracking and separation plant, reducing market risk around future expansion phases at that asset.

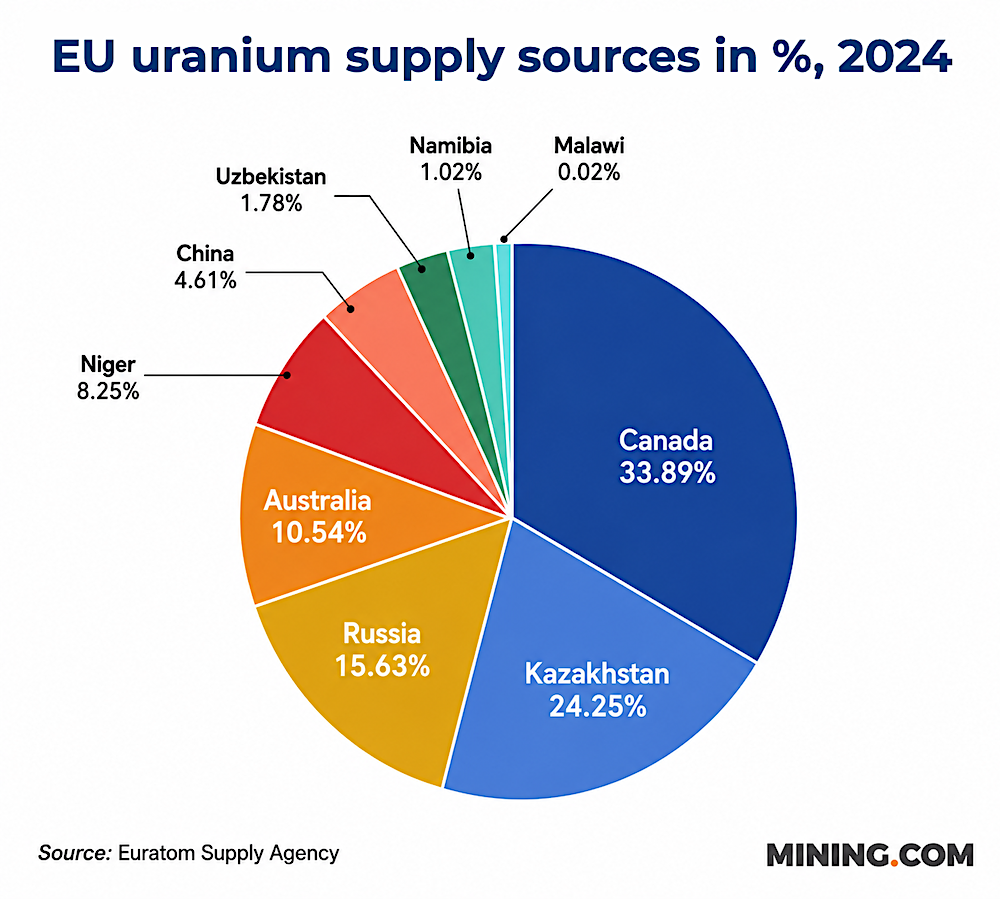

With Japan still sourcing 60–70% of its rare earths from China, locking in a US$110/kg NdPr floor price gives Lynas a planning base that most other non‑Chinese producers in our database (such as MP Materials and Energy Fuels’ White Mesa project) currently lack, which may influence where downstream magnet makers place new capacity.

Lynas’ A$20.7 billion market capitalisation and recent share price move position it as the clear scale leader among non‑Chinese rare earths in our coverage, which likely strengthens its hand in negotiating further offtakes for heavy rare earths beyond the 50% committed to JARE.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.