EU ban on Russian uranium: supply and contract outlook for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

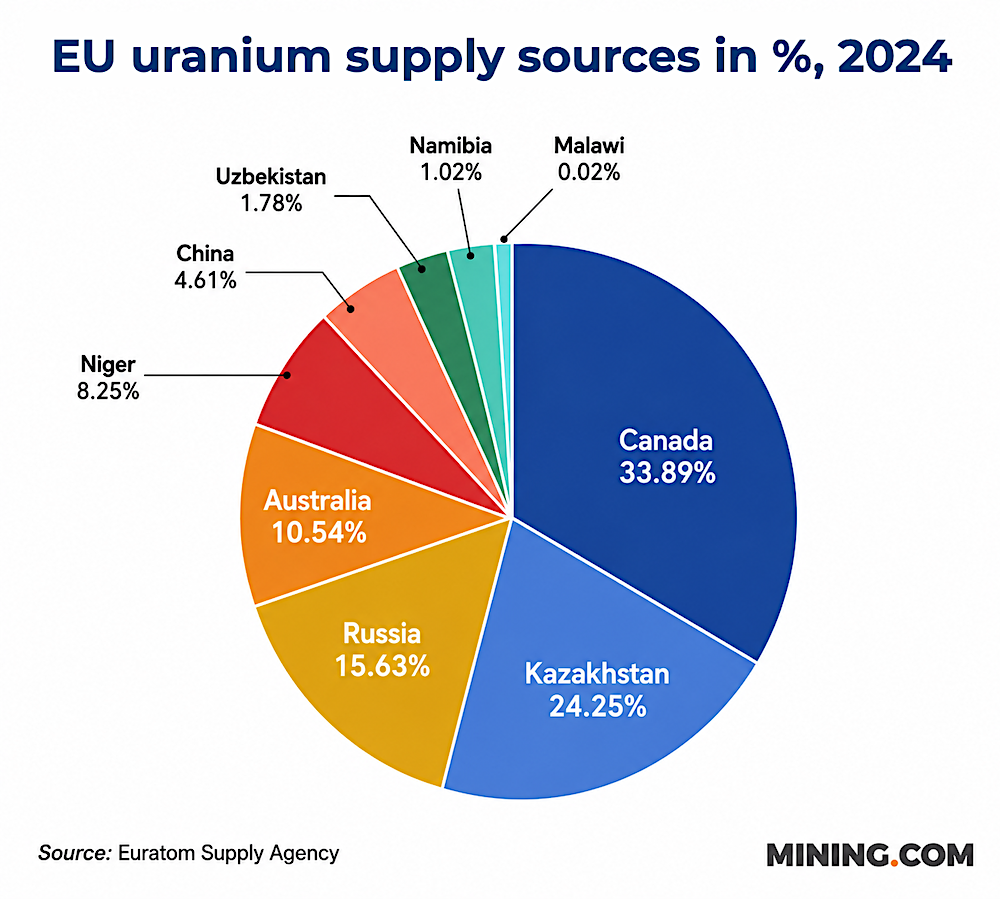

Mounting EU pressure to phase out Russian uranium and fuel services, which still provide about 25% of the bloc’s enrichment via Rosatom’s 43% share of global capacity, is pushing utilities towards Canadian supply, with Canada already covering more than 30% of EU uranium imports in 2024. Cameco, owner of 49% of Westinghouse, is positioned to capture long-term contracts as AP1000 reactor projects advance in Poland and Bulgaria and VVER units in Finland, Bulgaria, Slovakia and Ukraine convert to Western fuel. Analysts warn, however, that replacing Russian enrichment could take up to a decade due to limited Western capacity.

Technical Brief

- Rosatom currently controls about 43% of global uranium enrichment capacity, constraining rapid replacement options.

- Canada already supplied over 30% of EU uranium imports in 2024, becoming the bloc’s largest source.

- Cameco’s 49% stake in Westinghouse directly links its uranium portfolio to AP1000 reactor fuel contracts in Europe.

- Poland’s first nuclear plant and Bulgaria’s two planned Kozloduy AP1000 units underpin long-term Western fuel demand.

- Westinghouse fuel supply contracts now cover Soviet-designed VVER reactors in Finland, Bulgaria, Slovakia and fully in Ukraine.

- DiXi Group analysis suggests uranium mining supply can be diversified within a few years, unlike enrichment capacity.

- Replacement of Russian enrichment services is projected as a medium- to long-term (up to decade-scale) transition.

- The Rosatom-built Paks II project in Hungary remains a key outlier, with potential future political re-evaluation.

Our Take

Cameco’s 49% stake in Westinghouse positions Canada not just as a uranium ore supplier but as part of the EU-facing fuel fabrication chain, which in our database is unusual among raw-material exporters and gives it leverage in long-term utility contracting.

Canada already accounts for more than 30% of EU uranium imports in 2024, and in our coverage there are relatively few other uranium‑rich jurisdictions with comparable ESG and political‑risk profiles, which suggests higher bargaining power for Canadian producers on pricing and offtake terms.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.