Venezuela aluminium restart costs: WoodMac capex and risk lens for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

Reviving Venezuela’s vertically integrated aluminium chain would cost up to $2.3 billion, with Wood Mackenzie estimating $100–$200 million to restart the Los Pijiguaos bauxite mine to around 2 Mtpa, $500–$600 million to rehabilitate the Interalumina refinery to roughly 1 Mtpa, and $1–$1.5 billion to bring the 460,000 tpa Venalum smelter back online. BMI and BNEF stress that metal output has fallen over 90% since 2004, citing degraded infrastructure, chronic power instability at the Guri hydro complex, security risks and opaque regulation. Analysts warn that, despite 300 Mt of proved bauxite reserves and extensive inferred resources, political risk, sanctions exposure and faster, cheaper oil developments are likely to keep large-scale mining capital sidelined for at least a decade.

Technical Brief

- Venezuela’s aluminium output has fallen from >600,000 tpa peak capacity to effectively zero by 2025.

- US primary aluminium structural deficit exceeded 5 Mt in the last year, tightening regional supply options.

- Downstream producer Sural historically exported EC wire rod into North American and European power markets.

- Venezuela retains a hydro-powered, vertically integrated chain: bauxite mining, alumina refining and primary smelting.

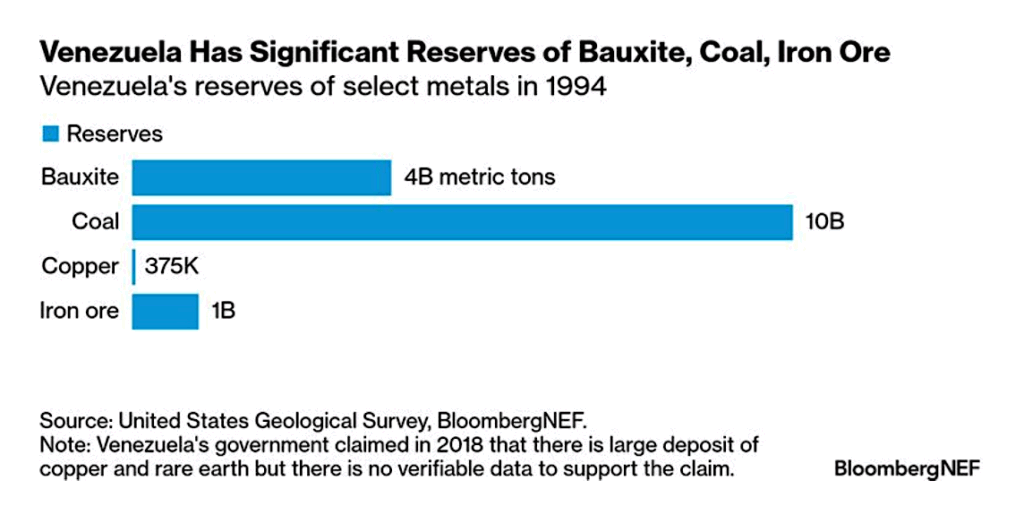

- Bauxite endowment includes >300 Mt proved reserves and up to 5,000 Mt inferred, comparable with top producers.

- Iron ore production has dropped from 20 Mt in 2004 to 2 Mt in 2024, indicating severe asset degradation.

- Bauxite output has declined from 5 Mt to 0.3 Mt, and coal from ~6 Mt to <0.5 Mt over 20 years.

- BMI projects Venezuela’s mining sector will remain among Latin America’s smallest and least attractive through 2035.

Our Take

BMI and Fitch Solutions appear across several recent pieces in our database on aluminium and broader industrial metals, signalling that the Venezuela restart analysis will likely be read alongside bullish 2026 price forecasts that could help justify high capex for assets like Los Pijiguaos and Interalumina.

With Venezuela’s bauxite output down from 5 Mt in 2004 to 0.3 Mt in 2024 and proved reserves of 300 Mt, the restart scenario effectively treats Bolívar and Amazonas as a long-life, underutilised resource base that could compete with West African and Australian supply if power reliability at the Guri hydro complex is demonstrably improved.

The US primary aluminium structural deficit of 5 Mt, highlighted in this piece, means any credible plan to bring Alcasa and Venalum back over a 2–3 year horizon would likely attract attention from North American offtakers seeking to diversify away from Chinese and Russian material, provided sanctions and political risk can be managed over the decade-long reform window.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.