Geopolitical shocks build copper’s bull case: supply–demand lens for mine planners

Reviewed by Tom Sullivan

First reported on MINING.com

30 Second Briefing

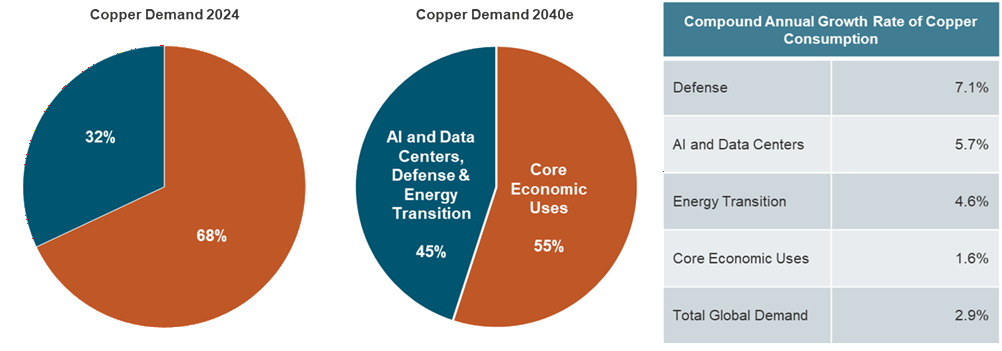

Geopolitical shocks from the US–Iran conflict are strengthening copper’s bull case, with Sprott analyst Jacob White forecasting that electrification, data centres and grid upgrades could lift these “strategic” uses from 32% of demand in 2024 to 45% by 2040, and noting this demand is less price-sensitive than construction. On the supply side, closure of the Strait of Hormuz has nearly doubled sulfuric acid prices, threatening SX-EW output that supplies about 4.8 Mt of copper and depends on sulfur flows from countries providing 49% of global sulfur trade. Despite higher sulfuric acid and diesel costs, Sprott says almost all copper mines remain profitable at the current US$13,000/t spot price, with copper equities already up 7.98% in April.

Technical Brief

- About 20% of global copper output uses SX-EW circuits that are directly dependent on sulfuric acid.

- Sprott estimates roughly 4.8 Mt/year of mine copper production is structurally tied to sulfuric acid supply.

- Closure of the Strait of Hormuz affects countries providing ~49% of internationally traded elemental sulphur feedstock.

- Since the US–Iran war began, benchmark sulfuric acid prices have almost doubled, raising SX-EW operating costs.

- Sprott notes production impacts from acid shortages will materialise over several months as inventories deplete.

- In the near term, copper producers are relying on stored and in-transit sulfuric acid to maintain leach operations.

- Elevated diesel prices are cited as an additional input cost pressure but not yet margin-destroying at current copper prices.

- Copper mining equities gained 7.98% in April, outperforming the underlying metal and other asset classes in Sprott’s tracking.

Our Take

Sprott’s recent launch of the Rare Earths Ex-China ETF, which also screens for exposure to sulphuric acid in critical-mineral supply chains, signals that the firm is already treating reagents like sulphuric acid as strategic inputs on par with metals such as copper and lithium.

With about 20% of global copper produced via SX-EW and nearly half of traded sulphur originating upstream of the Strait of Hormuz, any sustained disruption in that corridor would disproportionately hit low-grade leach operations, pushing capital towards sulphide concentrator projects less dependent on sulphuric acid.

Across our mining coverage, copper appears frequently alongside uranium, lithium and rare earths in Sprott-branded strategies, suggesting Sprott is positioning copper not just as a cyclical metal but as a core ‘energy transition’ asset class where geopolitical chokepoints like the Middle East are a key part of the investment thesis.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

Construction

Quality control software for construction companies with material testing, batch tracking, and compliance management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.