Mining deals hit $21.6B: key M&A and project signals for mine planners

Reviewed by Joe Ashwell

First reported on MINING.com

30 Second Briefing

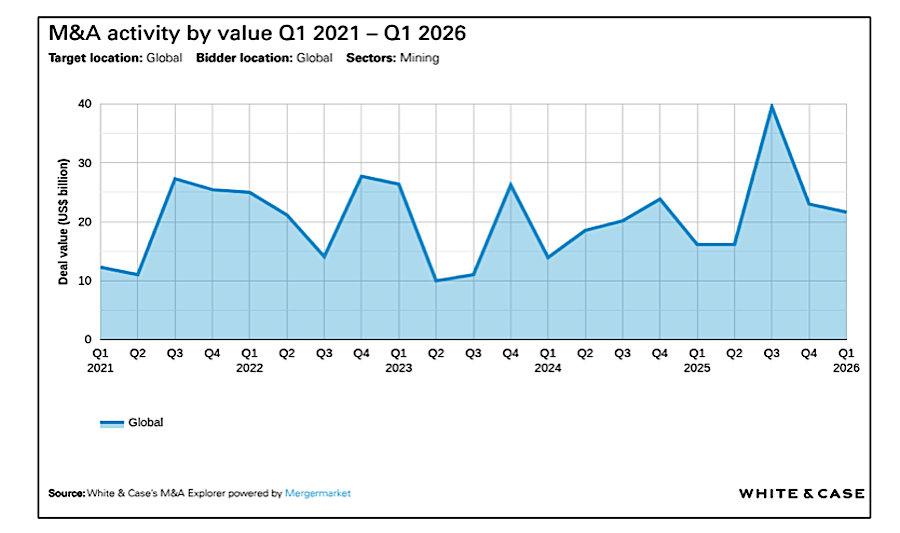

Global mining M&A reached $21.6 billion across 121 deals in Q1 2026, up 34% in value from Q1 2025 and 55% from Q1 2024, as capital pivots to critical minerals and stable jurisdictions despite the collapse of Glencore–Rio Tinto talks. White & Case’s 2026 Mining and Metals Survey reports 32% of respondents see strategic partnerships as the primary deal structure, exemplified by Serra Verde’s $565 million DFC financing and ~$2.8 billion combination with USA Rare Earth to build a mine-to-magnet rare earths chain outside Asia. Gold is flagged as the next consolidation hotspot as prices sit near record highs.

Technical Brief

- White & Case logged 121 mining M&A transactions in Q1 2026, versus 117 in Q1 2025.

- Deal count is also up from 102 transactions recorded in Q1 2024, indicating sustained activity.

- Full-year 2025 mining M&A totalled $93.7 billion, the highest annual value in 13 years.

- Glencore–Rio Tinto negotiations collapsed, yet aggregate sector deal value and volume still increased year-on-year.

- White & Case’s 2026 Mining and Metals Survey reports 32% of respondents favour strategic partnerships as the primary structure.

- Serra Verde’s US International Development Finance Corporation package totals $565 million, backing large-scale Brazilian rare earths development.

- Serra Verde’s roughly $2.8 billion combination with USA Rare Earth targets a mine-to-magnet supply chain outside Asia.

- Government-backed financing is described as increasingly co-investing alongside private capital in long-life, strategic mining projects.

Our Take

The prominence of critical minerals, rare earths and lithium in this Q1 2026 M&A data aligns with White & Case’s earlier 2026 survey, where nearly 40% of respondents expected state‑backed funding to be influential, signalling that deals like Serra Verde’s US International Development Finance Corporation package are likely to become a template for Brazil- and US‑linked projects.

With strategic partnerships identified by 32% of survey respondents as the most likely transaction form in 2026, combinations such as Serra Verde Group with USA Rare Earth suggest that mid‑tier players in rare earths and specialty minerals are increasingly using corporate tie‑ups rather than pure asset sales to secure downstream market access and funding certainty.

The planned A$2.05 billion‑scale graphite refinery at Baie‑Comeau underscores how Canada is emerging in our database as a preferred jurisdiction for large‑ticket battery‑materials processing, which may divert some future graphite and specialty minerals investment away from Australia despite its strong project pipeline.

Prepared by collating external sources, AI-assisted tools, and Geomechanics.io’s proprietary mining database, then reviewed for technical accuracy & edited by our geotechnical team.

Related Articles

Related Industries & Products

Mining

Geotechnical software solutions for mining operations including CMRR analysis, hydrogeological testing, and data management.

CMRR-io

Streamline coal mine roof stability assessments with our cloud-based CMRR software featuring automated calculations, multi-scenario analysis, and collaborative workflows.

HYDROGEO-io

Comprehensive hydrogeological testing platform for managing, analysing, and reporting on packer tests, lugeon values, and hydraulic conductivity assessments.

GEODB-io

Centralised geotechnical data management solution for storing, accessing, and analysing all your site investigation and material testing data.